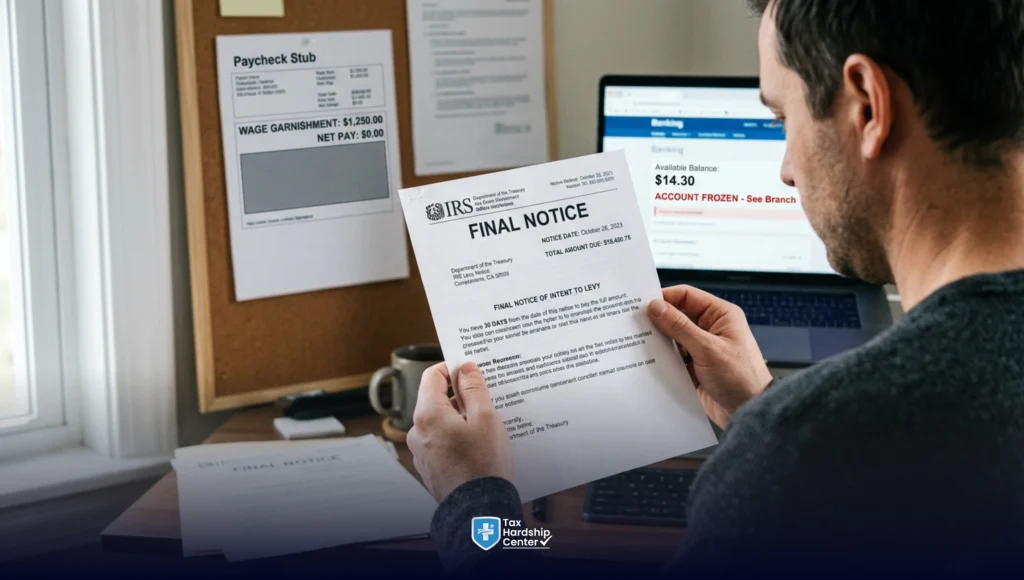

You opened a letter from the IRS, and the word “levy” is in the first paragraph. Your stomach dropped. You are not sure what a levy is, but you know it is no longer a warning. It is the IRS telling you they are about to take something.

A tax levy is the IRS’s legal seizure of your property to collect unpaid taxes. That property can be your wages, your bank account, your car, your house, or anything else you own that has value. A levy is not a threat. It is enforcement. By the time you receive a levy notice, the IRS has already sent you multiple warnings, and you are now at the final step before they take action.

This guide explains what a tax levy is, how it is different from a lien, what the IRS notice timeline looks like from first warning to final levy, what triggers a levy, the three ways to stop it before the IRS takes your paycheck or empties your bank account, and when professional help makes the difference between stopping the levy in time and losing financial control.

What a Tax Levy Is (and What It Is Not)

A tax levy is the IRS legally taking your property to satisfy unpaid tax debt. The IRS does not ask for permission. Once a levy is issued, they can seize wages, bank accounts, vehicles, real estate, retirement accounts, Social Security benefits, and other assets.

A levy is not a bill. A levy is not a warning. A levy is enforcement. It means the IRS has moved past sending notices and is now taking action to collect the debt.

The IRS has the legal authority to levy without going to court. They do not need a judgment. They do not need your consent. The authority comes from the Internal Revenue Code, which gives the IRS broad collection powers once specific procedural steps are completed.

What a levy does:

- Seizes your wages through continuous payroll deductions until the debt is paid

- Freezes and withdraws funds from your bank account

- Takes your tax refunds

- Seizes physical property like vehicles or real estate

- Offsets federal payments, including Social Security and veteran benefits

What a levy does not do:

- A levy does not just threaten to take action. It actually takes it

- A levy does not go away on its own. It continues until the debt is paid in full or you take action to stop it

- A levy does not require a court order. The IRS can issue a levy administratively after following the required notice procedures

The IRS only issues a levy after sending multiple notices over several months. If you just received your first balance-due notice, you are not at the levy stage yet. If you received a final notice with levy language and a right to a hearing, you are at the final step.

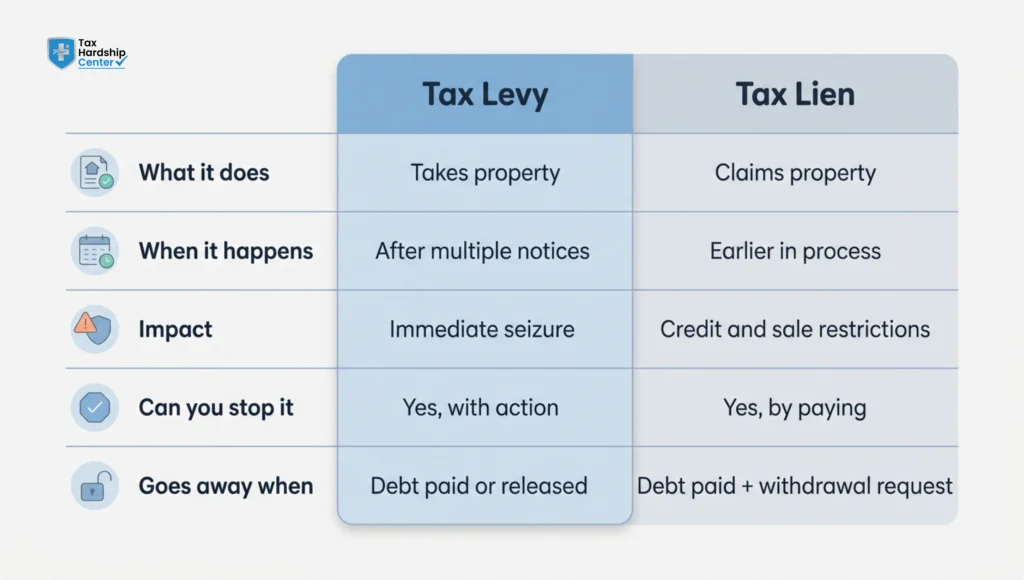

Tax Levy vs Tax Lien: What Is the Difference?

A levy and a lien are both IRS collection tools, but they work differently.

A tax lien is a legal claim against your property. It does not take your property. It attaches to everything you own and gives the IRS a legal interest in it. A lien makes it difficult to sell property, refinance loans, or get credit because the lien appears on your credit report and in public records. The IRS files a lien by recording a Notice of Federal Tax Lien with your county or state. Creditors, lenders, and anyone searching public records can see it.

A tax levy is the actual seizure of your property. The IRS does not just claim an interest in it. They take it. A levy can seize your wages, bank account, or physical assets. A levy happens after a lien is filed and after the IRS sends a final notice.

Timeline order: The IRS typically files a lien first, then issues a levy if the debt remains unpaid. You can have a lien without a levy, but you will almost always have a lien before a levy.

Which is worse: A levy is worse in terms of immediate financial impact because it takes your money or property now. A lien is worse in terms of long-term credit and financial reputation because it remains on your credit report and in public records even after the debt is paid, unless you request lien withdrawal.

For more on IRS liens and how long they last, see our guide on how long does an IRS lien last.

The IRS Notice Timeline Before a Levy Happens

The IRS does not issue a levy without warning. Federal law requires the IRS to send multiple notices before it can levy your property. Here is the typical notice timeline:

CP14 (First Notice): You owe a balance. This is the IRS informing you of unpaid taxes. You have 21 days to pay or set up a payment plan. No levy language yet.

CP501 (Second Reminder): You still owe a balance, and the IRS has not received payment or heard from you. This is a reminder. Still no levy threat. Learn more about CP501 IRS notice and your options.

CP503 (Third Reminder): The balance remains unpaid. The IRS is escalating. If you do not respond, the next notice will include levy language. See our guide on CP503 IRS notice meaning and next steps.

CP504 (Final Notice Before Levy on State Refund): The IRS intends to levy your state tax refund if you do not pay the balance or contact them within 30 days. This is where levy language first appears, but it applies only to your state refund, not to your wages or bank account yet. Read our detailed breakdown of CP504 IRS notice.

LT11 or Letter 1058 (Final Notice of Intent to Levy): This is the final warning. The IRS will levy your wages, bank account, or other property if you do not respond within 30 days. This notice includes your right to request a Collection Due Process (CDP) hearing. If you do not request a hearing or pay the balance within 30 days, the IRS can proceed with the levy without further notice.

The timeline from CP14 to the final levy notice typically spans 4 to 6 months. If you ignore every notice, the levy comes. If you respond at any point before the final notice, you can stop the levy by setting up a payment plan, requesting hardship status, or negotiating a settlement.

For more on what to do after receiving a final levy notice, see our guide on LT11 IRS notice and how to stop a levy.

What Triggers an IRS Levy

A levy does not happen just because you owe money. It happens because you owe money and have not responded to IRS notices or reached a resolution.

Unpaid tax debt for multiple months or years. The IRS does not levy immediately after you owe. They send notices first. If the debt sits unpaid for several months and you do not contact the IRS, they escalate.

Ignoring IRS notices. If you receive CP14, CP501, CP503, and CP504 notices and do not respond, the IRS assumes you will not pay voluntarily. They move to enforcement.

Defaulting on a payment plan. If you set up an installment agreement and then miss payments without contacting the IRS, they can issue a levy. Defaulting on a payment plan puts you back in enforced collection.

Not filing tax returns. If you owe tax and have unfiled returns, the IRS may file a Substitute for Return on your behalf and then immediately move toward levy because it views nonfilers as high-risk for collection.

The IRS believes you have the ability to pay but are choosing not to. If you are employed and receive regular wages or have money in a bank account, the IRS prioritizes those cases for levy because collection is straightforward. They levy on wages and bank accounts more often than on physical property because enforcement is faster and cheaper.

Types of IRS Levies: Wages, Bank Accounts, and Property

The IRS can levy different types of property depending on what you own and what is easiest to access.

Wage levy (wage garnishment)

The IRS sends a notice to your employer directing them to withhold a portion of your paycheck and send it to the IRS. A wage levy is continuous. It does not stop after one paycheck. The IRS takes a portion of every paycheck until the debt is paid in full or you take action to release the levy.

The amount the IRS can take from your wages is calculated based on your filing status and the number of dependents. For most single filers with no dependents, the IRS leaves you with roughly $400 to $800 per month to live on and takes the rest. For a married filer with two dependents, the exempt amount is higher, but the IRS still takes a large portion of your pay.

Wage levies are among the most common types of levies because they are easy to enforce and yield steady payments.

Bank levy

The IRS sends a levy notice to your bank. The bank freezes the funds in your account and holds them for 21 days. After 21 days, the bank sends the money to the IRS. A bank levy is a one-time seizure. If you deposit more money into the account after the levy is issued, the IRS does not automatically take it. They would need to issue a new levy.

Bank levies hit hard because the entire balance is frozen at once. If you have $5,000 in your account and the IRS levies it, that entire amount is frozen and sent to the IRS unless you take action during the 21-day hold period. Learn more in our guide on IRS bank levy release and how to stop account seizure.

Property levy

The IRS can seize vehicles, real estate, equipment, or other physical property. Property levies are less common because they require more effort. The IRS has to physically seize the property, store it, and sell it at auction. They usually levy on physical property only if the debt is large and other collection methods have failed.

Federal payment levy

The IRS can levy Social Security benefits, federal retirement payments, and other federal payments. They can take up to 15% of Social Security benefits to satisfy tax debt.

For more on how wage garnishment works and how much the IRS can take, see our guide on wage garnishment calculation.

Three Ways to Stop an IRS Levy Before It Happens

If you received a final levy notice (LT11 or Letter 1058), you have three options to stop the levy before it is issued.

Option 1: Pay the balance in full

If you pay the full amount owed, the IRS cancels the levy. This is the fastest way to stop enforcement. If you cannot pay the full balance, but you can pay a significant portion, call the IRS and negotiate. Paying down the balance may convince the IRS to delay the levy while you arrange a payment plan for the remainder.

Option 2: Set up a payment plan

If you cannot pay in full, apply for an installment agreement. You can apply online at IRS.gov if you owe $50,000 or less. If you owe more, call the IRS or submit Form 9465 with financial documentation. Once the payment plan is approved, the levy is released. The IRS will not levy if you are making regular payments under an approved plan.

For more on setting up a payment plan, see our guide on IRS payment plan options and how to apply.

Option 3: Request a Collection Due Process (CDP) hearing

The final levy notice includes information about your right to a CDP hearing. You have 30 days from the date on the notice to request a hearing. Requesting a hearing stops the levy while your case is reviewed by an IRS appeals officer. During the hearing, you can propose a payment plan, request an Offer in Compromise, or argue that the levy would cause economic hardship.

If you request a CDP hearing, the IRS cannot levy your property until the hearing process is complete. This buys you time to gather financial documentation, work with a tax professional, and negotiate a resolution.

If you miss the 30-day deadline to request a CDP hearing, you lose the right to stop the levy. At that point, the IRS can proceed with enforcement without further notice.

What Happens If the levy has already started

If the IRS has already levied your wages or bank account, you can still take action to get the levy released.

Pay the balance in full. If you pay the debt, the levy is released immediately.

Set up a payment plan. Even after a levy is issued, you can apply for an installment agreement. Once the payment plan is approved, the levy is released. This is the most common way people stop an active levy.

Request a levy release due to economic hardship. If the levy is preventing you from paying for basic living expenses like rent, utilities, or food, you can request a levy release based on economic hardship. You will need to submit Form 433-A or Form 433-F with documentation of your income and expenses. The IRS will review your financial situation and determine whether to release the levy.

Request Currently Not Collectible (CNC) status. If you genuinely cannot afford to pay anything right now because your income only covers necessary living expenses, you can request CNC status. The IRS pauses collection efforts while you are in CNC. The levy is released, but the debt still exists, and interest continues to accrue.

Wait for the 21-day bank levy hold period. If the IRS levied your bank account, the bank holds the funds for 21 days before sending them to the IRS. You have 21 days to take action. If you set up a payment plan or prove economic hardship during that 21-day window, the levy can be released, and the funds returned to your account.

For wage levies, release is not automatic even after you set up a payment plan. You may need to call the IRS and request that they send a levy release notice to your employer. Processing the release can take 1 to 2 weeks.

Why Professional Help Matters When You Receive a Final Levy Notice

An LT11 or Letter 1058 is the IRS’s final warning before a levy. Once that notice arrives, you usually have just 30 days to act before the IRS can garnish wages or freeze your bank account.

A lot of taxpayers lose time trying to figure out the right move first, whether that is a payment plan, hardship request, or CDP hearing, while the deadline keeps running. And if you miss that 30-day window, the IRS can move forward with the levy even if you are still trying to resolve the case.

Things get even harder when unfiled returns, rejected payment plans, or missing financial documents are involved. Many people do not realize the IRS may reject a low monthly payment proposal if they believe you can afford more.

Tax Hardship Center helps taxpayers stop levies before they begin and release levies that have already been initiated. The firm files Collection Due Process hearing requests within the deadline, negotiates payment plans or settlements, and submits hardship documentation when clients cannot afford to pay.

For bank levies, acting during the 21-day hold period is critical. For wage garnishments, the goal is usually to get a payment agreement in place quickly enough to secure a levy release.

If you received a final levy notice or your wages or bank account have already been hit, getting professional help quickly can make a major difference before the situation gets worse.

FAQs

What does it mean when you levy a tax?

When the IRS levies, it means they are legally seizing your property to collect unpaid tax debt. The levy can take your wages, bank account, tax refund, or physical assets like vehicles or real estate. A levy is not a warning. It is enforcement.

How serious is an IRS levy?

An IRS levy is the most aggressive collection action the IRS can take. It immediately impacts your ability to pay bills, cover rent, and buy groceries. A wage levy continues until the debt is paid in full or you take action to stop it. A bank levy freezes your account and takes the entire balance after 21 days. Levies do not go away on their own.

Why do I have a tax levy?

You have a tax levy because you owe unpaid tax debt, and the IRS sent you multiple notices that went unanswered or unresolved. The IRS does not levy without warning. If you ignored notices or did not set up a payment plan, the IRS will collect the debt by force.

How do I stop a levy from the IRS?

If you received a final levy notice, you can stop it by paying the balance in full, setting up a payment plan, or requesting a Collection Due Process hearing within 30 days. If the levy has already started, apply for a payment plan or request a levy release based on economic hardship. Once a payment plan is approved, the levy is released.

How long before the IRS issues a levy?

The IRS sends multiple notices over a 4- to 6-month period before issuing a levy. The typical timeline is CP14, CP501, CP503, CP504, and then LT11 or Letter 1058 (final notice). If you do not respond to the final notice within 30 days, the IRS can levy your property without further warning.

What triggers an IRS levy?

An IRS levy is triggered by unpaid tax debt, ignoring IRS notices, failing to set up a payment plan, defaulting on an existing payment plan, or having unfiled tax returns. The IRS levies when they believe voluntary compliance has failed and enforcement is the only way to collect the debt.

Conclusion

A tax levy is the IRS taking your property to collect unpaid taxes. It is not a warning. It is enforcement. By the time you receive a final levy notice, the IRS has already sent you multiple reminders and given you months to resolve the debt voluntarily. If you ignore the final notice, the levy will be assessed.

The notice timeline is predictable. CP14, CP501, CP503, CP504, and then LT11 or Letter 1058. At every step before the final notice, you have the option to stop the levy by paying the balance, setting up a payment plan, or requesting hardship status. Once you receive the final notice, you have 30 days to request a Collection Due Process hearing or take action to resolve the debt. After that, the IRS can levy without further warning.

If the levy has already started, you can still get it released. Set up a payment plan, prove economic hardship, or request Currently Not Collectible status. The levy does not have to stay in place forever. But it does not stop on its own. You have to take action, and in most cases, you have to act fast.

Key Takeaways:

- A tax levy is the IRS’s legal seizure of your property to collect unpaid taxes. It takes your wages, bank account, or other assets

- A levy is different from a lien. A lien is a claim against your property. A levy is the actual seizure of it

- The IRS sends multiple notices over a 4- to 6-month period before issuing a levy. The final notice is LT11 or Letter 1058

- You can stop a levy by paying the balance in full, setting up a payment plan, or requesting a Collection Due Process hearing within 30 days of the final notice

- Wage levies are continuous and take a portion of every paycheck until the debt is paid. Bank levies freeze your account and take the entire balance after 21 days

- If a levy has already started, you can get it released by setting up a payment plan or proving economic hardship

- The 30-day window to request a CDP hearing is firm. Missing it means the levy proceeds without further notice

If you received a levy notice or a levy has already been issued, get a free case review at Tax Hardship Center.