You’re 68 years old. Your only income is Social Security and a small pension. The IRS says you owe $18,000 from years when you still worked or took early withdrawals from retirement accounts. The letters keep coming, and you’re terrified they’ll take your Social Security check or the small savings account you use for bills.

Here’s what most seniors don’t realize: the IRS has specific rules about what it can and cannot collect from people on fixed retirement income. You might qualify for relief that pauses collections entirely, reduces what you owe, or spreads payments across a timeline that actually matches your income.

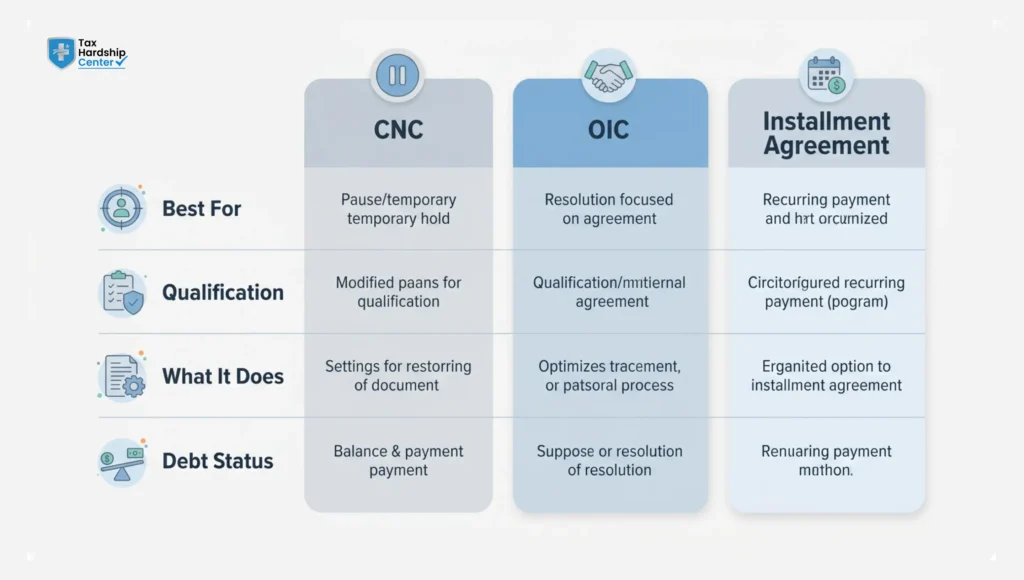

The three main options are Currently Not Collectible status (CNC), Offer in Compromise (OIC), and installment agreements. Each one fits a different financial situation. The IRS does not advertise which one you qualify for. They wait for you to ask, and if you ask for the wrong one, they will deny you and move forward with enforcement.

This guide explains how each option works, who qualifies, and how the IRS decides which path fits your situation.

Does the IRS Offer Special Tax Forgiveness Just for Seniors?

No. The IRS does not have a program called “senior tax forgiveness.” There is no age-based exemption that wipes out tax debt once you turn 65.

What the IRS does have are relief programs available to all taxpayers, and some of those programs work particularly well for seniors on fixed income because the eligibility rules center on your ability to pay rather than your age.

According to the IRS’s own collection guidelines, the agency is required to consider a taxpayer’s financial situation before pursuing aggressive enforcement, which often works in favor of seniors with limited and fixed income sources.

The three programs seniors use most often are:

Currently Not Collectible (CNC) status stops IRS collections when your income barely covers necessary living expenses. The IRS temporarily suspends enforcement, but the debt does not disappear and interest continues to accrue.

Offer in Compromise (OIC) settles your debt for less than you owe if the IRS determines you will never be able to pay the full amount based on your income, expenses, and assets.

Installment agreements spread your tax debt across monthly payments. If you can afford a small monthly payment but not a lump sum, the IRS will set up a plan that keeps you in compliance.

Each option requires you to provide documentation of your financial situation. The IRS does not take your word for it. They want Social Security statements, pension statements, bank statements, and a detailed breakdown of your monthly expenses.

Currently Not Collectible Status: When Your Income Barely Covers Basics

CNC status tells the IRS you cannot pay anything right now. Your income is too low, and after covering rent, utilities, food, and medical expenses, there is nothing left for the IRS.

The IRS grants CNC when your allowable monthly expenses equal or exceed your monthly income. They do not use your actual expenses. They use their own allowable expense standards, which are based on national and local data. If you spend $800 on groceries and the IRS standard is $500, they only count $500.

Who Qualifies for CNC Status

You are a strong candidate if any of the following apply:

- Your only income is Social Security, SSI, or a small pension

- You have no assets the IRS can levy, meaning no home equity and no savings beyond a minimal emergency fund

- Your monthly income does not cover IRS allowable living expenses

- You are facing financial hardship due to age, health issues, or disability

What Happens When You Get CNC Status

The IRS stops all collection actions. They will not levy your bank account, garnish your income, or file new liens. Existing liens remain in place, but the IRS will not enforce them while you are in CNC.

Your debt does not disappear. Interest continues to accrue. The IRS reviews your status every two years. If your financial situation improves, they will restart collections.

CNC works well for seniors who genuinely cannot pay and do not expect their income to increase. If you are 72 and living only on Social Security, your income will not change significantly. CNC can effectively pause collections indefinitely in those circumstances.

The statute of limitations continues to run while you are in CNC status. The IRS has 10 years from the date it assessed your tax to collect it. If that 10-year window expires while you are in CNC, the debt becomes legally uncollectible and drops off entirely.

How to Apply for CNC Status

Submit IRS Form 433-F (Collection Information Statement) or Form 433-A if your finances are more complex. The form asks for your income, expenses, assets, and liabilities.

Include the following documentation with your submission:

- Social Security benefit statement

- Pension statements

- Bank statements for the last three months

- Rent or mortgage statement

- Utility bills

- Medical expense records

The IRS compares your income to its allowable expense standards. If expenses meet or exceed income, they will grant CNC status.

If you need help with the application, our back tax resolution services include preparing and submitting CNC requests on your behalf.

Offer in Compromise: Settle for Less Than You Owe

An Offer in Compromise lets you settle your tax debt for less than the full amount owed. The IRS agrees to accept a lump sum or short-term payments that total less than your full balance.

The IRS approves an OIC only when it believes it will never collect the full amount. They calculate your “reasonable collection potential” based on your income, expenses, and assets. If that number is lower than your tax debt, you may qualify.

Who Qualifies for an OIC

You are a candidate for an OIC if:

- Your income is low and unlikely to increase significantly

- You have minimal assets, meaning no home equity and only small retirement accounts

- You cannot afford an installment agreement that would pay off the debt within the 10-year collection statute

- Paying the full debt would create severe and lasting economic hardship

Most seniors who own a home with significant equity will not qualify. The IRS includes home equity in its calculation. If you have $50,000 in equity, they will expect you to access it through a loan or a sale before they consider a settlement.

If your only assets are a modest retirement account and your home has little to no equity, an OIC becomes far more realistic.

How the IRS Calculates Your Offer Amount

The IRS uses the following formula:

Reasonable Collection Potential = (Monthly Disposable Income x 12 or 24) + Asset Equity

Disposable income is your monthly income minus allowable expenses. If you have $200 left over each month after allowable expenses, the IRS multiplies that amount by 12 months for a lump-sum offer or by 24 months for a payment plan offer. Then they add your accessible asset equity.

If your total tax debt is $30,000 but your reasonable collection potential is $8,000, the IRS may accept an $8,000 offer to close the account.

The OIC Application Process

You submit Form 656 (Offer in Compromise) along with Form 433-A (Collection Information Statement). You also pay a $205 application fee and an initial payment. If you qualify for the Low Income Certification, both the fee and initial payment are waived.

The IRS takes 6 to 12 months to review your offer. During that time, collections are paused. If they accept, you pay according to the agreed terms. If they reject, you can appeal or pivot to requesting CNC status. For a full walkthrough of the process, see our guide on how the Offer in Compromise works.

Installment Agreements: Spread Payments You Can Actually Afford

If you cannot pay your tax debt in full but can afford monthly payments, an installment agreement keeps you in compliance and stops IRS enforcement actions from escalating.

Types of Installment Agreements

Short-term payment plan: You owe less than $100,000 and can pay in full within 180 days. No setup fee and no formal agreement paperwork required.

Long-term payment plan (Streamlined Installment Agreement): You owe $50,000 or less and can pay within 72 months. The IRS approves most streamlined requests without requiring detailed financial documentation.

Partial Payment Installment Agreement (PPIA): You owe more than you can pay within the collection statute. The IRS accepts monthly payments based on what you can afford, knowing the full balance will not be paid before the statute expires. The remaining debt is forgiven when the statute runs out.

Who Should Choose an Installment Agreement

An installment agreement fits your situation if:

- You have income beyond Social Security, such as a pension, part-time work, or rental income

- You can afford a monthly payment between $25 and $200

- You want to avoid liens and levies while remaining compliant

- Your income slightly exceeds your allowable expenses, so CNC does not apply

An installment agreement is typically the easiest option to get approved. The IRS would rather receive consistent small payments than spend resources pursuing an OIC dispute or CNC review.

How to Set Up a Payment Plan

If you owe less than $50,000, apply online through the IRS payment plan portal. The setup fee ranges from $31 to $225, depending on your payment method, with direct debit being the least expensive option.

If you owe more than $50,000, you will need to submit Form 433-F or 433-A with supporting financial documentation. The IRS will calculate a monthly payment based on your disposable income. Once approved, make payments on time. A missed payment defaults your agreement and restarts enforcement. Our team can help you structure a plan through our IRS payment plan services.

Can the IRS Garnish Social Security or Your Pension?

The IRS can garnish Social Security benefits for tax debt, but the amount is limited. They can take up to 15% of your Social Security benefit through the Federal Payment Levy Program (FPLP). This is a federal program specifically authorized for tax debt collection, which is why it operates differently from how other creditors operate. Other creditors cannot touch Social Security, but the IRS can.

However, the IRS typically does not pursue Social Security garnishment if you qualify for CNC or have an approved OIC or payment plan in place.

Pensions are fully subject to IRS levy. If you have pension income, the IRS can garnish it the same way they garnish wages. The amount they take depends on your filing status and number of dependents, but it is generally more aggressive than the 15% Social Security cap.

If you are already in an approved payment plan or CNC status, or have submitted an OIC, the IRS suspends levy actions during the review period. If you are facing active garnishment, see our guide on stopping IRS wage garnishment for immediate steps you can take.

According to a Social Security Administration overview of benefit protections, federal tax debts are one of the few exceptions to the general rule protecting Social Security payments from garnishment.

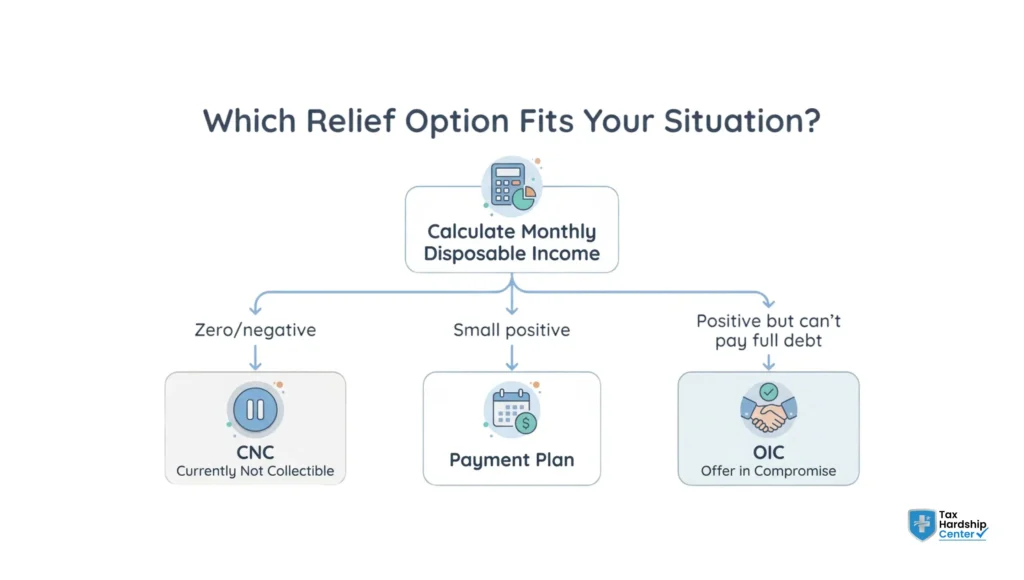

How to Choose the Right Relief Option

Use this decision framework based on your actual monthly financial picture.

Pursue CNC status if:

- Your only income is Social Security or a very small pension

- You have no savings or accessible assets beyond basic necessities

- Your monthly income does not cover IRS allowable living expenses

- You are not working and do not plan to return to work

Pursue an Offer in Compromise if:

- You have a low income and minimal assets

- You can access a lump sum through family assistance, selling an asset, or borrowing

- You do not own a home with significant equity

- Paying the full debt over 10 years is financially impossible, given your income

Pursue an installment agreement if:

- You have income beyond Social Security, such as a pension, part-time work, or rental income

- You can afford a monthly payment between $25 and $200

- You want to stay compliant and avoid enforcement actions

- Your income slightly exceeds your allowable expenses, so CNC does not fit

If you are not certain which path applies, start by calculating your monthly disposable income. Subtract your allowable living expenses from your monthly income. If the result is zero or negative, CNC is your path. If it is positive but small, an installment agreement fits. If it is positive but you will never pay off the full debt within 10 years, an OIC is worth pursuing.

How the Tax Hardship Center Helps Seniors Navigate IRS Relief

When you are managing tax debt on Social Security or a fixed pension, the process of identifying and applying for the right IRS relief program is not straightforward. Tax Hardship Center works specifically with seniors facing collection concerns, handling Currently Not Collectible applications for those whose income does not cover IRS allowable expenses, preparing Offer in Compromise submissions when income and asset levels support settlement, and structuring installment agreements designed around fixed retirement income.

Many seniors who come to us have multiple years of unfiled returns, late-filed returns that triggered penalty abatement opportunities, or situations where retirement account distributions created unexpected tax liability no one explained to them at the time. We also handle cases where a senior fell behind due to health issues, cognitive decline, or reliance on a family member who did not file correctly. In those situations, reasonable cause penalty abatement can reduce the total balance owed before any resolution program is even applied.

For seniors who cannot manage IRS correspondence independently due to mobility or health limitations, or who find IRS notices overwhelming, we handle everything: document collection, financial statement preparation, direct communication with the IRS, and follow-up on applications and appeals. If you want to understand which option fits your situation before committing to anything, get a free case review, and a specialist will walk you through your income, expenses, and which relief path makes the most sense for your specific circumstances.

FAQs

Who qualifies for tax forgiveness for seniors?

There is no special IRS forgiveness program based only on age. Seniors qualify for relief programs based on income, assets, and ability to pay.

Does the IRS go after senior citizens?

Yes. The IRS can still pursue collections, but taxpayers on fixed income with limited assets may qualify for less aggressive resolution options.

Can the IRS garnish my Social Security?

Yes, but there are limits. In many cases, taxpayers who qualify for hardship programs can reduce or avoid collection actions altogether.

How do you qualify for tax forgiveness?

You qualify by showing the IRS that paying the full balance would create financial hardship based on your income, expenses, and assets.

What is the $6,000 tax credit for seniors?

This usually refers to proposed tax relief measures tied to larger standard deductions for older taxpayers, not direct forgiveness of existing tax debt.

At what age does the IRS stop collecting back taxes?

The IRS does not stop collections because of age alone. Most tax debts remain collectible until the legal collection period expires.

Is there any way to get taxes completely forgiven?

Some taxpayers qualify for settlement programs or hardship status that can reduce or eliminate collection activity over time.

How much will the IRS usually settle for?

The IRS bases settlements on your realistic ability to pay, including your income, expenses, and available equity in assets.

Conclusion

The IRS does not have a special forgiveness program for seniors. What they do have are three relief options that work for people on fixed income: Currently Not Collectible status, Offer in Compromise, and installment agreements.

If your income barely covers rent, utilities, food, and medical expenses, CNC status pauses collections. If you can access a lump sum and your income and assets are low, an OIC might settle your debt for significantly less than you owe. If you can afford a small monthly payment, an installment agreement keeps you compliant and stops enforcement.

The IRS does not volunteer this information. You have to ask. If you ask for the wrong option, they will deny you and move forward. If you qualify for relief and do not apply, levies and garnishments will follow.

Start by documenting your income and expenses. Calculate your monthly disposable income. That single number points you toward the right path.

Key Takeaways

- The IRS offers no age-based forgiveness program, but seniors on fixed income frequently qualify for CNC status, OIC, or installment agreements based on their limited ability to pay

- CNC status stops all collection actions when the monthly income does not cover IRS allowable living expenses, and the debt expires if the 10-year statute runs out during that period

- An Offer in Compromise settles your debt for less than you owe when the IRS calculates your reasonable collection potential is below your total balance

- The IRS can garnish up to 15% of Social Security benefits through the FPLP, but rarely pursues it when a CNC or payment plan is already approved

- Pensions are fully subject to IRS levy and can be garnished more aggressively than Social Security if no resolution is in place

- You must apply for relief and document your financial situation; the IRS will not offer these options on its own

- The correct relief option depends on one number: your monthly disposable income after IRS allowable expenses

- Penalty abatement can reduce your total balance before any resolution program is applied, which is especially relevant for seniors who fell behind due to health or circumstances

- Home equity is included in OIC calculations and can disqualify seniors who otherwise appear to have low income

- Filing all unfiled returns is a required first step before the IRS will consider any resolution option, including CNC or OIC