Your business didn’t pay its debts. So why is the IRS sending letters to your house?

That’s the moment most business owners first hear about the Trust Fund Recovery Penalty, and it’s usually the worst possible way to hear about it. One day you’re dealing with a struggling company. Next, the IRS is treating it as if you personally owe the money, not the business. If that sounds like a plot twist nobody warned you about, that’s because almost nobody does.

The Letter That Turns a Business Problem Into a Personal One

Here’s how it usually starts. Cash gets tight. Payroll is due Friday. The IRS deposit for withheld payroll taxes is also due, and something has to give. So you pay your crew, your vendors, your rent, and you tell yourself you’ll catch up on the payroll tax deposit next quarter.

Reasonable decision. Wrong debt to skip.

That withheld money, the income tax and FICA you pulled from every employee’s paycheck, was never really yours. You were just holding it for the IRS. The IRS calls it “trust fund” money for exactly that reason, and when it doesn’t show up, they don’t just chase the business. They come looking for the person who decided not to send it.

What the Trust Fund Recovery Penalty Actually Is

The Trust Fund Recovery Penalty, or TFRP, is the IRS’s way of collecting unpaid payroll taxes directly from an individual instead of the business entity. It exists because a corporation or LLC can shield an owner from most business debts, but the IRS decided decades ago that payroll trust fund money would be the exception.

Under Internal Revenue Code Section 6672, the IRS can assess a penalty equal to 100 percent of the unpaid trust fund taxes against any person it determines was “responsible” and acted “willfully” in failing to pay. Not 50 percent. Not a fraction tied to your role. The full amount, assessed against you as an individual, separate from whatever happens to the business.

That’s the twist nobody explains upfront: this isn’t a business penalty with your name attached. It’s a personal tax bill.

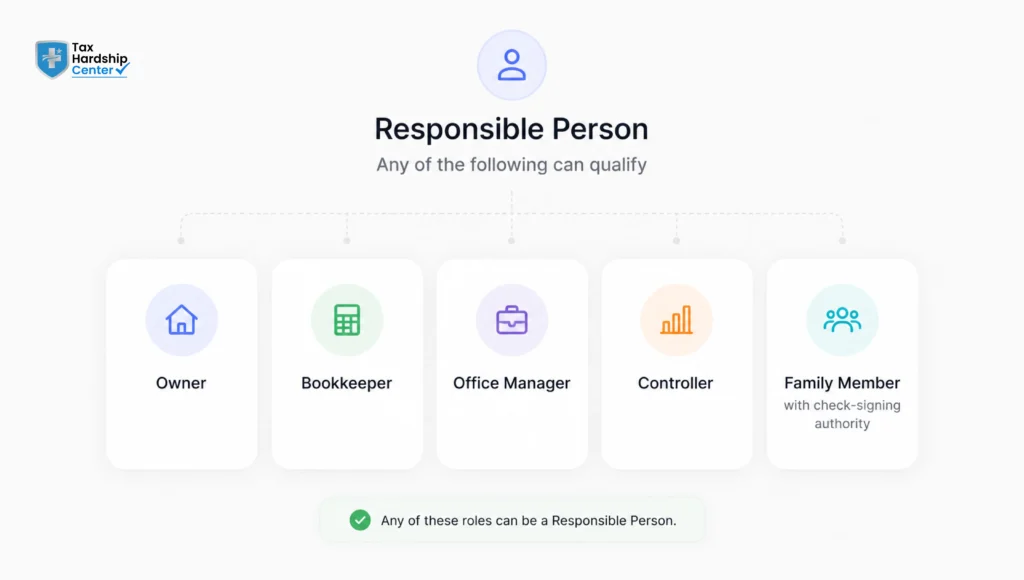

Who Counts as a “Responsible Person” (Hint: It’s Not Just the Owner)

This is where most business owners get blindsided. They assume the IRS is only looking at whoever signed the incorporation papers. The IRS’s own guidance describes a responsible person as someone required to collect, account for, and pay over trust fund taxes, who willfully fails to do so.

In practice, that net is wide. It can include the CEO, a bookkeeper, an office manager, a controller, or even a family member who wasn’t drawing a salary but had check-signing authority. The IRS doesn’t care about your job title. It cares about who actually had control over which bills got paid.

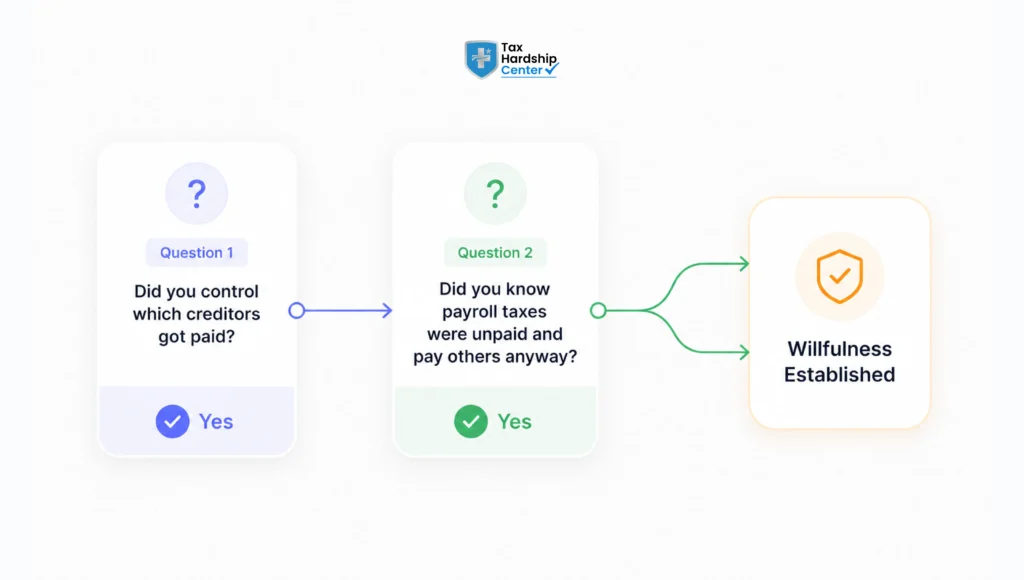

The Two Questions the IRS Actually Asks

Every TFRP investigation comes down to two questions, and they’re less about your title and more about your leverage.

Did you have the authority to decide which creditors got paid, the IRS or someone else? And did you know the payroll taxes were unpaid, and did you choose to pay other obligations anyway? If both answers are yes, willfulness doesn’t require bad intent. Choosing payroll and rent over the IRS is enough.

Inside Form 4180: How the IRS Decides Who Pays

Before the IRS assesses this penalty against anyone, a revenue officer usually conducts what’s called a 4180 interview, named after the form they use to document it. It feels like a routine conversation. It is not.

The interview walks through who had signature authority on the bank accounts, who decided which invoices got paid, who prepared or reviewed payroll tax returns, and who had the power to hire or fire the person handling payroll. Every answer builds a case, and once that case is built, the IRS can name more than one responsible person for the same unpaid taxes. That’s not a typo. Multiple people can be assessed the full 100 percent, and the IRS collects from whoever pays first, then leaves those individuals to sort out contribution claims among themselves.

Why This Penalty Hits Different

Most tax debt has an exit ramp. This one barely does.

The TFRP generally survives bankruptcy, meaning filing Chapter 7 or Chapter 13 typically will not erase it. It attaches to you personally, which means it can lead to a federal tax lien on your house, your car, your personal bank accounts, regardless of what happens to the business. And because it’s assessed against an individual rather than an entity, closing the business, walking away, or starting a new company under a different name does nothing to make it disappear.

This is the part that turns a cash flow decision made on a stressful Friday afternoon into a multi-year personal financial problem.

Mistakes That Turn Suspicion Into an Actual Assessment

Many business owners make this worse without realizing it, often by trying to handle the 4180 interview alone. Answering casually, without understanding how each answer maps to the willfulness test, can turn an ambiguous case into a clear one.

Others assume that because they’ve since resigned, sold the business, or handed payroll duties to someone else, they’re automatically off the hook. Responsibility is based on the period the taxes went unpaid, not your current role. And some owners wait too long to respond to IRS notices at all, which lets the case move toward assessment on the government’s timeline instead of theirs.

What You Can Do Before and After Assessment

If you haven’t been assessed yet, the goal is to control the narrative before the 4180 interview happens, not after. That means understanding exactly who had check-signing authority during the periods in question and documenting it, before you’re in a room answering questions under pressure.

If the penalty has already been assessed, you still have options. You can request an appeal within the timeframe on your notice. You can pursue an installment agreement or, in some cases, an offer in compromise on the TFRP amount itself. And if more than one person was assessed, understanding who actually controlled the money matters for any contribution claim down the line.

Why Business Owners Choose Tax Hardship Center for TFRP Cases

If you’re staring at a 4180 interview request or an assessment notice, this is not the moment to wing it with a generic tax preparer. Trust fund recovery cases are personal liability cases, and the questions asked in that interview determine what you owe for years. Tax Hardship Center handles these cases specifically, not as an afterthought attached to general back tax help.

Our business services team handles payroll tax cases as they actually unfold, coordinating with your existing CPA rather than working around them, and preparing owners for the 4180 interview before the IRS asks its first question. If the case has already moved past assessment, we walk through resolution paths including installment agreements and offer in compromise eligibility, so you know which path actually fits your situation, not just the one that sounds best in an ad.

For business owners still catching up on payroll deposits and trying to avoid a TFRP case altogether, our small-business IRS payment plan guide and overview of full tax debt relief options break down what’s realistic before the situation escalates to personal liability.

FAQs

Can the IRS really come after me personally for payroll taxes?

Yes. Under Section 6672, the IRS can assess the Trust Fund Recovery Penalty against any individual it determines was responsible and willful in failing to pay over withheld payroll taxes, separate from the business’s own liability.

What does “willful” actually mean in a TFRP case?

It does not require intent to defraud. Knowing the taxes were due and choosing to pay other creditors instead is generally enough to meet the willfulness standard.

Can more than one person be held liable for the same unpaid taxes?

Yes. The IRS can name multiple responsible persons for the same trust fund taxes, and each can be assessed the full amount, though the government only collects the total once.

Does filing for bankruptcy eliminate the Trust Fund Recovery Penalty?

Usually not. The TFRP is generally treated as a nondischargeable debt in both Chapter 7 and Chapter 13 bankruptcy filings.

I already resigned from the company. Am I still at risk?

Possibly. Liability is based on your authority during the periods the taxes went unpaid, not your current title or employment status.

What happens during the Form 4180 interview?

An IRS revenue officer asks detailed questions about who controlled the bank accounts, who decided which bills got paid, and who managed payroll tax filings, building the case for who is responsible.

Can I negotiate the amount after the penalty is assessed?

In some cases. Options can include appeals, installment agreements, or an offer in compromise specifically on the TFRP amount, depending on your financial situation.

Get a free case review with Tax Hardship Center today.

Conclusion

The Trust Fund Recovery Penalty exists because the IRS treats withheld payroll money differently from other business debts, and once a case moves toward assessment, it stops being about the business entirely. The earlier you understand where you stand, before the 4180 interview instead of after, the more control you have over the outcome.

Key Takeaways

- The Trust Fund Recovery Penalty lets the IRS collect unpaid payroll taxes directly from an individual, not just the business

- Responsible person status depends on authority over payments, not job title

- The IRS can assess the full 100 percent against more than one person for the same unpaid taxes

- The Form 4180 interview is where most TFRP cases are effectively decided

- Willfulness does not require bad intent; choosing other bills over the IRS is enough

- The TFRP generally survives bankruptcy and personal liens

- Resigning or closing the business does not remove liability for prior unpaid periods

- Waiting to respond to IRS notices lets the case move on the government’s timeline

- Appeals, installment agreements, and offer in compromise are still options after assessment

- Preparing before the 4180 interview matters more than reacting after it