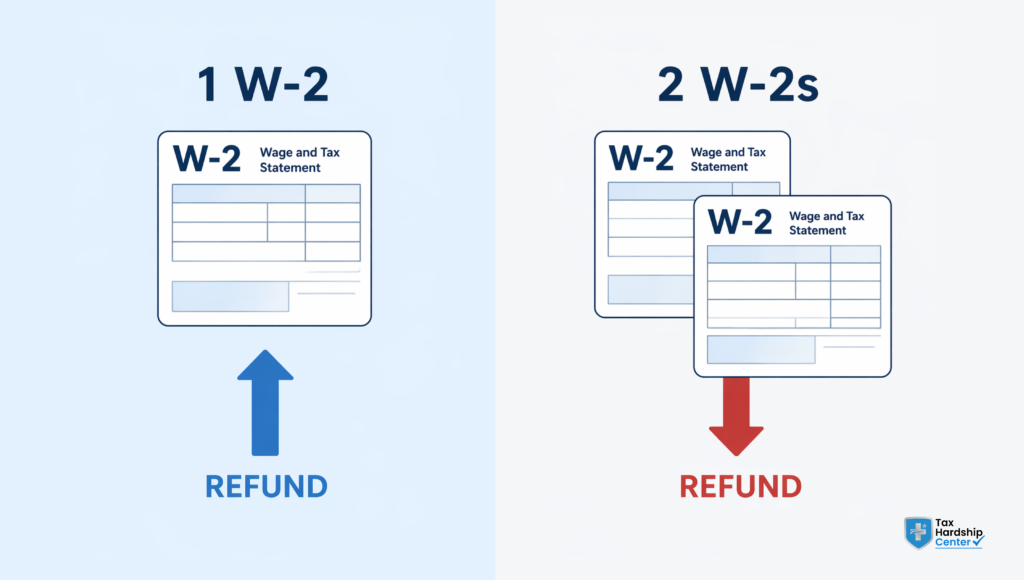

You were following along in your tax software, refund number climbing, feeling good about it. Then you added the second W-2. The refund dropped. Maybe by a few hundred dollars. Maybe by a few thousand.

Your first reaction is probably that something went wrong. It didn’t. But here’s what actually happened, and why it matters more than most people realise.

Why Your Refund Exists in the First Place

A tax refund is not a bonus. It’s your own money coming back to you because your employer withheld more than you actually owed.

Every paycheck, your employer sends a portion of your wages directly to the IRS. That amount is based on a withholding calculation tied to the information you put on your Form W-4. At tax time, the IRS tallies up what you actually owed based on your total income for the year. If you overpaid through withholding, you get a refund. If you underpaid, you owe the difference.

That’s it. The refund is just the gap between what you paid in and what you actually owed.

What Changes When You Add a Second W-2

Here is where people get confused.

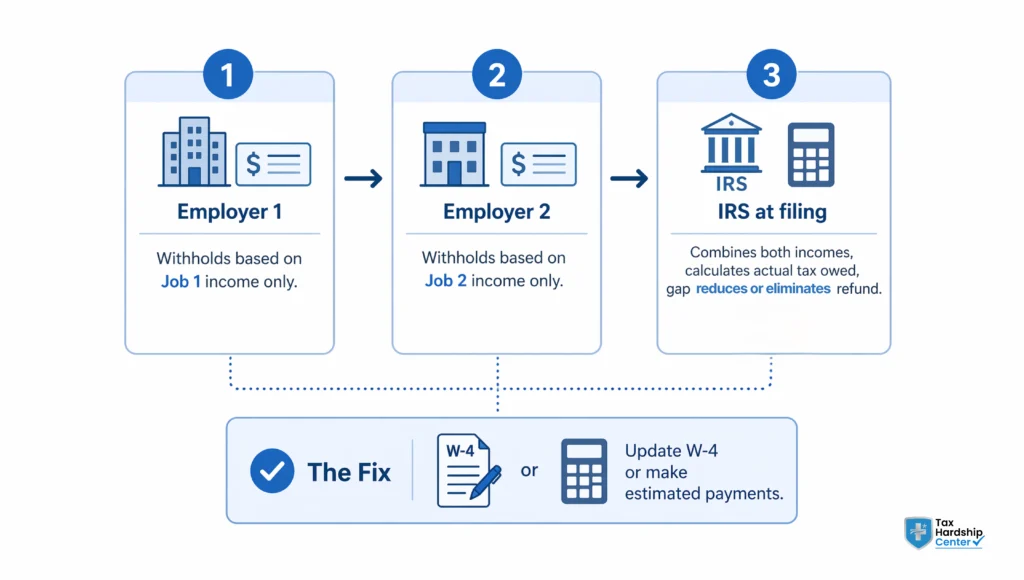

Each employer withholds taxes as if the job they’re paying you for is your only job. Your first employer looks at your W-4 and calculates withholding based on, say, $40,000 a year. Your second employer does the same thing independently. They have no idea about the first job.

The problem is that the United States federal income tax uses a progressive tax bracket system. The more you earn in a year, the higher the rate on the dollars above each threshold.

When you have two jobs, your combined income pushes some of your earnings into a higher bracket. But neither employer withheld at that higher rate. They each withheld at the rate appropriate for a lower income level.

So when your tax software sees the full picture, it recalculates your actual tax liability based on your total combined income. The result is usually a higher tax bill than either the W-4 predicted. That’s why the refund drops.

It’s not a glitch. It’s math working correctly for the first time.

The Withholding Problem Nobody Warned You About

Let’s put real numbers to this.

Say your first job paid you $38,000. Your employer withheld taxes as if that were your annual income. You were on track for a decent refund.

Then you added a second W-2 for $14,000 from a part-time job or seasonal work. Your total income is now $52,000. Depending on your filing status, some of that $14,000 gets taxed at 22% instead of 12%. But your second employer withheld at the lower rate because they only saw $14,000.

The gap between what your second employer withheld and what you actually owed on that income is what eats your refund. In this example, that could easily be $800 to $1,400 less than you were expecting.

The same logic applies if you added a spouse’s W-2 to a joint return. Their employer withheld based solely on their income. Your combined income may push the household into a higher bracket.

This is not your tax software making a mistake. It’s showing you the accurate number for the first time.

When a Smaller Refund Becomes a Real Tax Bill

A smaller refund is annoying but not a problem.

An actual balance owed can become one if it’s large enough or if it happens repeatedly without being addressed.

If you underpay your taxes by more than $1,000 in a year and did not pay enough through estimated payments or withholding, the IRS may charge an underpayment penalty. For 2024 and 2025, that penalty rate has been running between 7% and 8% annualized, calculated on the shortfall.

If you owe a balance at filing and don’t pay it, the IRS begins charging interest from the due date. Balances that go unaddressed can grow into formal collection situations, CP14 notices, and eventually enforcement action.

Most people who find themselves in IRS collections did not start with a massive debt. They started exactly here: a tax return that came back with a balance they didn’t have money to pay, so they filed and hoped for the best. Then the same thing happened the following year.

If your refund dropped significantly and you now owe a balance for this year or any prior year, that’s worth dealing with directly rather than ignoring. You can learn more about your options on our IRS payment plan and installment agreement guide.

How to Fix Withholding Going Forward

The good news: this is fixable before it becomes a real problem.

The IRS Tax Withholding Estimator at IRS.gov/W4app lets you enter your total income from all sources and calculate what your actual tax liability will be. From there, you can see whether your current withholding across all jobs is enough.

If it’s not, you have two options.

The first is to submit a new W-4 to one of your employers to request additional withholding. There’s a line on the W-4 specifically for this: Line 4(c), which lets you request a flat additional dollar amount withheld each pay period. Even adding an extra $50 or $75 per paycheck from your main job can eliminate a year-end balance.

The second option is making estimated quarterly payments directly to the IRS. This is more relevant if you have 1099 income in addition to W-2 income, but it also applies to W-2 workers. Estimated payments are due four times a year and cover the shortfall your withholding doesn’t catch.

Either way, the goal is to get your total withholding and estimated payments close to what you’ll actually owe, so you’re not caught off guard at filing.

If you’ve already fallen behind on taxes from prior years where this situation played out, and the balance grew, take a look at our overview of help with back taxes and IRS relief options.

How the Tax Hardship Centre Can Help

If adding a second W-2 reduced your refund to zero or created a balance you weren’t expecting, Tax Hardship Centre can help you understand exactly where you stand with the IRS and what your options are.

THC works with individuals who have W-2 income, 1099 income, or both. If you’ve had multiple jobs across one or more years and aren’t sure whether you’ve been withholding correctly, a free case review will tell you whether you have a balance, whether any penalty relief applies, and what the most realistic path forward looks like.

THC does not promise specific outcomes. What it does is give you an honest answer about your situation before asking you to commit to anything. That includes reviewing your IRS account, explaining what any balance means for your filing status, and walking through payment options if you need them.

FAQs

Why did my refund go down when I added a second W-2?

Each employer withholds taxes based only on the income they pay you. When your second W-2 is added, your total income may push some earnings into a higher tax bracket. Neither employer accounted for that, so your actual tax liability is higher than what was withheld.

Do multiple W-2s hurt your tax return?

They don’t hurt your tax return in a permanent or punitive way, but they can reduce your refund or create a balance owed if your combined withholding wasn’t enough to cover your total tax liability for the year.

Is it better to have more withheld at my main job if I have two jobs?

Yes. You can submit a new W-4 to your primary employer and use Line 4(c) to request additional withholding per paycheck. This is the simplest way to correct under-withholding without managing estimated quarterly payments.

What happens if I owe a balance I can’t pay by the filing deadline?

File your return on time even if you can’t pay in full. Filing late adds a separate penalty to the balance. Once filed, you can apply for an IRS instalment agreement to pay the balance over time. See our installment agreement guide for specifics.

Can this situation lead to IRS collection problems?

Yes, if an unpaid balance grows across multiple years without being addressed. The IRS sends a sequence of notices beginning with a CP14. If those are ignored, the situation escalates toward liens, levies, and wage garnishment. Catching and addressing a balance early is always the lower-cost path.

Does adding a spouse’s W-2 cause the same refund drop?

It can, yes. When you file jointly, your combined income determines your tax bracket. If your spouse’s employer withheld at a rate calculated only on their income, and your household’s combined income puts some of their earnings in a higher bracket, the same gap occurs.

Is the IRS Tax Withholding Estimator accurate?

It’s reasonably accurate if you enter your information completely, including all income sources, filing status, deductions, and credits. It won’t account for every individual situation perfectly, but it gives a solid estimate of whether your withholding is tracking correctly for the year.

Conclusion

A lower refund after adding a second W-2 is not a mistake. It’s the result of each employer withholding independently at a rate calculated for lower-income earners, while your combined income pushes part of your earnings into a higher tax bracket.

The refund drop reflects the gap between what was withheld and what you actually owed. In most cases, the fix is to adjust your W-4 at one or both jobs to request additional withholding, or to make estimated quarterly payments to cover the shortfall.

If the gap resulted in a balance you couldn’t pay, or if this has happened across multiple years, the problem is worth addressing now rather than waiting for IRS notices to escalate. The sooner it’s addressed, the more options you have.

Get a free case review at taxhardshipcenter. If you have a balance from a prior year or aren’t sure where you stand with the IRS, speak to a tax specialist today.