Tax forgiveness program basics sit under the IRS Fresh Start initiative, which groups real relief tools like installment agreements, offers in compromise, penalty abatement, and currently not collectible status. You qualify when you file all required returns, stay in good standing, document financial hardship, and choose a payment plan or settlement that fits your budget. You can pay over time with a simple online plan, settle for less through an offer in compromise when your ability to pay falls short, or ask the IRS to delay collection if you cannot pay anything now. The IRS now lets you check eligibility, make payments, and even file an offer in compromise in your Online Account, which shortens the paperwork and gives clear status updates. Keep reading to learn who qualifies, what each relief option does, how the application works, and what happens after the IRS decides.

Who Qualifies for IRS Fresh Start Relief

Fresh Start relief favors taxpayers who act fast, file on time, and share complete financial information. The IRS checks whether you filed all required returns for the last years, whether you made estimated payments if you are self-employed, and whether you have a current balance that fits an installment agreement, offer in compromise, or a temporary delay. You improve your odds when you show a clean filing record, a clear picture of income and necessary expenses, and a budget that supports either monthly payments or a realistic settlement. You also need to stop new debts from piling up by adjusting withholding or quarterly estimates so you do not create a new balance while you ask for relief. With those basics set, you can move into one of the core forgiveness programs that reduce penalties, spread payments, or settle for less based on your ability to pay.

Eligibility Essentials

Filing Status, Income, and Qualifications

Eligibility income drives several decisions. Your tax filing status and marital status set standard deductions and show household size, which affects the budget the IRS accepts. Track gross income, including unemployment benefits, side hustle receipts, and state taxes withheld, because those inputs power your forms and any low-income certification. The IRS tests qualifications with math, not guesses, so keep ledgers and bank statements that support every figure. If you change filing status after a life event, update your plan right away so the payment still fits.

Eligibility Essentials

You qualify for Fresh Start relief only when you stay current on filings and payments going forward. File all past-due returns and correct missing information so the IRS can calculate your true balance and evaluate your request. Keep your federal tax deposits and quarterly estimates current if you run a business, and fix your Form W-4 or quarterly vouchers so you do not create a new balance while in a plan. The amount you owe also steers you to the right program: streamlined installment agreements fit many balances, while offers in compromise apply when your reasonable collection potential falls below what you owe. A sharp drop in income or a spike in necessary expenses strengthens a claim for a lower monthly payment or a settlement; for example, a self-employed filer who shows a 25 percent revenue decline year over year signals clear hardship when the books support it.

Low-Income and Innocent Spouse Considerations

Low-income certification matters across several relief programs. If your income falls within published thresholds, the IRS may waive the offer in compromise application fee and initial payment, which lowers the cash you need to start a settlement. Low-income status can also reduce installment agreement setup fees and make direct debit the cheapest route to stay compliant. Innocent spouse relief protects a spouse who did not know, and had no reason to know, about errors or omissions on a joint return that created the tax debt. You apply with the facts, show what you knew at the time, and document control of the household finances to support your claim. When the IRS grants relief, it shifts part or all of the joint liability off the innocent spouse, which can open a path to a plan or settlement on the remaining balance for the other filer.

Use spouse clearing language when you explain how the debt arose and who controlled the records. A licensed representative can act on your behalf and submit documents through the IRS website or secure fax, then share confirmation details so you can track progress.

What If You Don’t Qualify?

If you apply and do not qualify for one program, you still have options. The IRS may steer you to a different path based on the same financials, such as a streamlined installment agreement instead of an offer in compromise. You can request Currently Not Collectible status when your budget shows that you cannot pay anything after basic living costs; that pause stops most enforcement while interest and penalties continue to add to the balance. You can also request penalty abatement when you meet first-time abatement rules or when reasonable cause fits your facts, such as documented illness, disaster loss, or records destroyed by theft. If none of those fit, you can adjust withholding and estimates, set a short-term plan to pay within 180 days, and avoid liens or levies by showing that you are acting in good faith.

Advocate and Bankruptcy Considerations

Contact the Taxpayer Advocate Service when systemic issues block relief. TA case teams handle a wide range of problems, which many call TA Tax Diversity, and they drive cases that need urgent attention. Ask about TA Tax Forgiveness coordination when delays piled for tax forgiveness across several years. As a last resort, review bankruptcy proceedings with counsel. Some income taxes can discharge if you meet strict timing rules on filing, assessment, and age of the debt. Bankruptcy never erases payroll trust fund taxes, and it can affect liens, so treat it as a legal decision with clear pros and cons.

Our Services at Tax Hardship Center

Our services at Tax Hardship Center focus on plain-English planning, accurate paperwork, and steady contact with the IRS. When a monthly plan fits, we set up a direct debit Installment Agreement that matches your cash flow and keeps you compliant. If a settlement makes more sense, we prepare and file an Offer in Compromise with full documentation and status updates. For complex cases that span multiple years, we organize returns, bank records, and budgets so your eligibility stands on solid numbers. You stay in control while our team handles the details through your IRS account and our IRS Tax Relief service.

Understanding Tax Debt Forgiveness Options

The Fresh Start umbrella covers several tools that reduce the pressure of IRS tax debt and move you toward resolution. Installment agreements stretch payments over time with known monthly amounts and fewer touch points. Offers in compromise let you settle for less than the full amount when your assets and income cannot cover the liability within the collection window. Currently Not Collectible status pauses enforced collection because you cannot meet basic expenses if you pay, yet it requires you to stay current on new filings. Penalty abatement cuts or removes failure-to-file or failure-to-pay penalties when first-time or reasonable cause standards apply. Together these options give you a structured way to protect wages and bank accounts, manage cash flow, and reach final resolution without guesswork.

$1 You can set up an Installment Agreement with our team and compare plan types in our blog, Understanding IRS Payment Plans.

If You Can Pay Part of Your Balance

Tailor your monthly payment to what you can afford after necessary expenses such as housing, utilities, food, insurance, and transportation. Direct debit plans cost less to set up and help you avoid missed payments, which keeps liens and levies off your back. If you owe more than a basic threshold, direct debit may be required, so open a checking account if you do not have one. When your cash flow improves, you can increase your monthly amount to shorten interest and penalty costs. Keep new taxes current during the plan so the IRS does not terminate the agreement for a new balance.

If You Can’t Pay Anything Now

If your budget leaves no room after basic living costs, ask the IRS to delay collection and place your account in Currently Not Collectible status. You will show income, necessary expenses, and asset equity so the IRS sees that payment would cause hardship. The IRS pauses most collection actions while you are in CNC, but interest and penalties continue to accrue and the IRS may keep future refunds to reduce the debt. You must file returns on time while in CNC and report changes when your income rises, because the IRS can review your case and restart collection if your ability to pay improves. CNC does not erase the debt; it gives you breathing room while you stabilize finances.

$1

Read our Offer in Compromise service and deep dives on IRS Form 656 and OIC eligibility before you start.

Submit your application (Form 656, Form 433-A/OIC)

Complete Form 656 to state your offer and the tax periods you want to settle, and complete Form 433-A/OIC or 433-B/OIC to show assets, income, and expenses. Include the application fee and the initial payment unless you meet low-income certification, which waives both. Choose between a lump-sum offer or a periodic payment plan, and send supporting documents such as bank statements, pay stubs, mortgage or lease papers, and proof of necessary expenses. Keep copies of everything and track deadlines so you respond fast to any IRS request for more information. If you file online through your IRS account, you can monitor status and make required payments in one place.

Online Resources and Confirmation

Use the IRS Offering Compromise Booklet for line-by-line help and examples. The web application inside your Online Account walks you through inputs and produces a confirmation number after each payment or upload. Save those confirmations and screenshots from the website with your case file.

If your offer is accepted or rejected what comes next

If the IRS accepts your offer, follow your payment schedule exactly, file on time for five years, and avoid any new unpaid balances. The IRS will remove related liens after you satisfy the terms of the offer and pay the full agreed amount. If the IRS rejects your offer, you can appeal within the deadline on the letter and you can pivot to another relief option such as a partial payment installment agreement. Review the rejection reasons, fix documentation gaps, and consider a revised offer if your financials change. Do not ignore a rejection letter; act quickly so you keep control of the timeline and protect your paycheck and bank account.

Currently Not Collectible (CNC) Status

CNC status applies when you cannot pay anything after necessary living costs and payment would cause hardship. You document income and expenses with a Collection Information Statement so the IRS can see the gap between what comes in and what must go out. The IRS pauses most enforcement once it approves CNC, which means no active wage garnishment or bank levy while the status remains. Interest and penalties continue to add up, and the IRS may keep refunds and certain credits during CNC to reduce your balance. You regain control of cash flow right away, but you must stay current on new filings and tell the IRS when your income changes. Document financial distress with bills, eviction notices, medical statements, or shutoff warnings when available. These proofs support hardship and speed a CNC decision.

$1

If penalties stand in the way, our Penalty Abatement service and this step-by-step blog, How to Dispute an IRS Penalty, show what to file and when.

$1

If payroll hits feel close, see our Wage Garnishment page and this blog on IRS tax levies.

State Taxes and Offsets

Fresh Start rules apply to federal balances. State taxes follow their own hardship programs, forms, and clocks. Many states honor federal payment plans when you share approval letters. The IRS applies any overpayment to past-due taxes or other federal debts under the Treasury Offset Program, even while you sit in a plan or CNC.

Step-by-Step Process: How to Apply

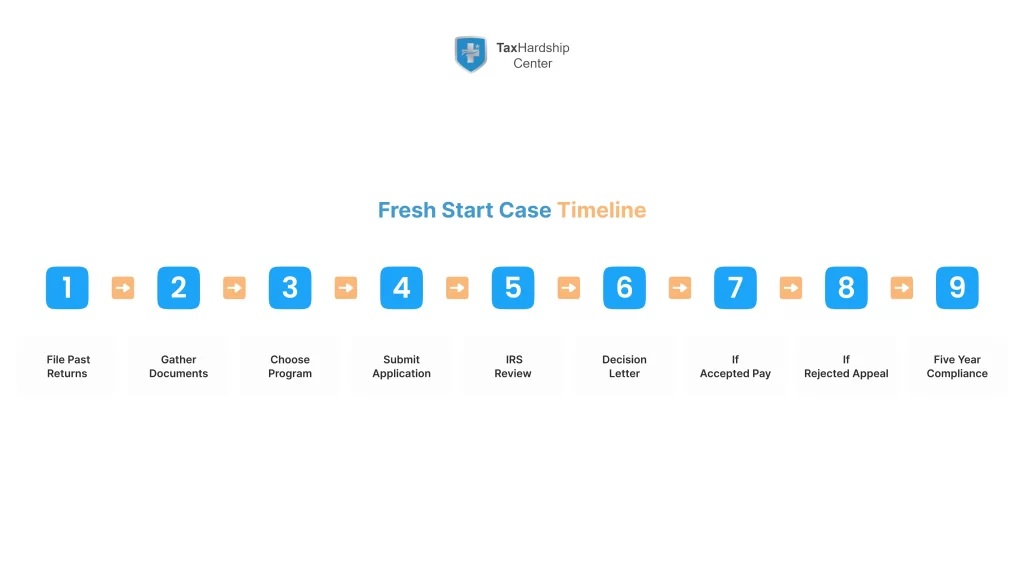

You move faster and face fewer surprises when you follow a clear checklist. Start by filing missing returns and fixing withholding or estimates so you stop new debt from forming. Pull your bank statements, pay stubs, mortgage or rent details, and bills for necessary expenses so you can complete forms cleanly. Choose the program that fits your budget and your balance, and use online tools where available to cut down on mail delays. Track every deadline and respond to IRS letters on time to keep your case moving. When in doubt, speak with a qualified tax attorney or enrolled agent to confirm the numbers and present your case clearly.

Prepare and Select Your Payment Option

Begin with filing compliance and a realistic budget. Decide whether a short-term payment plan within 180 days solves the problem or whether you need a longer installment agreement. If your assets and income cannot reach the balance within the collection period, you can evaluate an offer in compromise; if you cannot pay anything now, consider CNC. Match your choice to your real numbers, not to wishful thinking, because the IRS will test your math against bank records, pay stubs, and other documents. Direct debit plans usually cost less and reduce risk of default, and low-income certification can cut fees and upfront costs in several programs.

$1

For official forms and eligibility tools, use the IRS Offer in Compromise page and the IRS Get Help with Tax Debt hub.

Understand the Process

Expect a review period where the IRS checks your forms and may ask for more information. Watch your mail and your Online Account for requests or decisions, and answer quickly with complete documents. During review, stay current on any estimated taxes or required deposits so you do not create a new problem while the old one gets solved. If the IRS approves a plan, make every payment on time and automate it when possible; if the IRS needs more details, send them before the deadline on the notice. You control the outcome when you stay organized and proactive through each step.

Outcomes: What Happens After Submission

IRS decisions fall into a few clear buckets, which each trigger next steps. An accepted offer in compromise locks in the settlement amount and a schedule you must follow, plus a five-year compliance window you must respect. An approved installment agreement sets a monthly payment that you must meet each cycle, with default if you miss or add new debt. A CNC approval stops most enforcement while interest and penalties continue to grow, and the IRS will review your case later to see if your ability to pay changed. A rejection pushes you to appeal, adjust your documentation, or select another program based on the same facts. Each outcome still demands that you file returns on time and avoid new balances so you do not lose the relief you earned.

If Your Offer Is Accepted

An accepted offer delivers finality when you complete the payments and stay compliant for five years. Pay on schedule, keep your filings current, and avoid any new debt so the IRS does not default the offer. Ask about lien release or withdrawal once you complete the terms so public records reflect your new status. Use the fresh start to reset your withholding or quarterly estimates and build a simple budget that keeps you on track. Keep a folder with the acceptance letter and proof of payment for your records, because lenders may ask for it when you apply for credit.

If Your Offer Is Rejected

A rejection does not end your path to relief. Read the reason codes, fix gaps in documentation, and file an appeal by the deadline on the letter if you believe the decision missed key facts. If your numbers do not support an offer, pivot to a partial payment installment agreement that meets your budget or seek CNC if you cannot pay anything. You can also request penalty abatement to bring the total down to a manageable level that fits a plan. Keep communication open and do not ignore notices, because silence invites liens and levies.

Overpayments and Refunds

Expect the IRS to keep future refunds and any earned overpayment until you satisfy the balance or the statute runs. Plan cash flow so refund capture does not derail your monthly bills.

Protect Yourself: How to Avoid Tax Relief Scams

Tax relief scams target people who feel pressure to resolve a large balance fast. Bad actors advertise a “one-time forgiveness” that promises debt wiped clean with no documents or math, then demand upfront fees that deliver no results. Watch for sales reps who dodge questions about IRS forms and who refuse to discuss budgets or documentation, because real cases run on numbers you can prove. Avoid firms that guarantee acceptance of an offer in compromise or claim special connections inside the IRS. Always verify credentials and ask for a written scope of work that lists the forms, timelines, and fees before you sign anything.

Extra Protections When Using a Representative

A tax attorney or enrolled agent files a power of attorney and communicates on your behalf. Require written confirmation of every submission and payment. Work through secure portals on the firm’s website or through your IRS account, not email attachments.

Common Scams and Red Flags

Be wary when a company promises full debt forgiven without reviewing bank records, pay stubs, and asset lists. Do not share bank account numbers or credit card details with a caller who refuses to explain the specific forms they will file for you. Avoid contracts that hide extra fees, demand large retainers without a plan, or block you from contacting the IRS directly. Hang up on any caller who threatens arrest or immediate asset seizure, because the IRS does not operate by phone demands or social media messages. You protect yourself when you insist on written explanations and you check every claim against information you can confirm.

Working with Legitimate Tax Attorneys or Enrolled Agents

A licensed tax attorney or enrolled agent will explain each program, run the numbers with you, and communicate with the IRS under a signed power of attorney. Ask for experience with offers in compromise, installment agreements, CNC, and penalty abatement, and request a plain-English roadmap with milestones and fees. Many reputable firms, including Tax Hardship Center, offer a free consultation that screens your case and outlines realistic outcomes before you commit. Professionals help you avoid errors on Forms 656, 433-A/OIC, or 9465, assemble documents the IRS expects, and keep your case moving during review. You still make the decisions, but you gain a guide who keeps the math honest and the deadlines tight.

How IRS Fresh Start Relief Helps You

Fresh Start relief aims to stop the spiral of penalties and interest while you regain control of your finances. Installment agreements replace panic with a predictable monthly payment you can handle. Offers in compromise give you a clean end point when your assets and income cannot satisfy the full balance within the collection period. CNC status protects basic living expenses when payment would force you below a reasonable standard. Penalty abatement rewards clean filing history or documented reasonable cause by cutting fees that serve no purpose once you get back on track.

Hardship Programs During Unemployment

Job loss changes eligibility income. When unemployment hits, update your budget and request lower payments or CNC. Share proof of benefits, job search records, and cutbacks. Many households can still qualify for first-time penalty abatement while between jobs if they fix filings and enter a plan. Relief programs exist to help you bridge the gap and keep current.

Benefits of IRS Forgiveness Program

Tax relief options cut penalties, spread payments, and settle balances based on what you can actually afford. Flexible payment plans fit seasonal income swings and help self-employed filers who face uneven cash flow. Offers in compromise pair strict documentation with true hardship and can settle a large balance for an amount that reflects your real ability to pay. Penalty abatement reduces the drag on your payoff schedule and can turn an impossible total into a plan you can finish. Together these tools reduce pressure, protect assets, and deliver a path to resolution you can see from day one.

$1

Smart Documentation and Budgeting Tips for Approval

Strong files win relief. Build a truthful budget with bank statements, pay stubs, leases, insurance bills, and proof of child care or medical costs. Map every line to IRS Collection Financial Standards so an agent can test your math in minutes. Show how you cut nonessential spending and why the remaining costs meet local norms. Add a one-page overview that explains the story behind the numbers so the reviewer sees need, not guesswork.

Build a Truthful Budget

List net pay, gross income, side gigs, and unemployment. Track cash deposits and payment apps so totals match your bank activity. Flag seasonal swings if you run a small business and attach month-by-month profit and loss. Your budget should show you can keep the plan or why you need settlement or CNC. Honest math beats wishful thinking every time.

Use Allowable Expense Standards Wisely

The IRS allows national and local standards for food, clothing, housing, utilities, and transportation. If your actual cost runs higher for a necessary reason, provide documents and a short note that explains why. Do not pad numbers. Show bids for cheaper insurance or a smaller car payment to prove you looked for savings. Aligning with standards improves speed and acceptance.

Asset Equity and Quick Sale Values

Offers and partial payment plans factor asset equity at quick sale value. Provide statements for mortgages, car loans, retirement accounts, and any business equipment. Explain why certain tools count as necessary for work. If you have a tax lien, note how it limits refinance options and raises your cost of funds. The equity math sets the floor for any offer in compromise.

Track Confirmation and Case Notes

Use the IRS website and your Online Account to upload documents and send secure messages. Save each confirmation number and date in a simple log. When a representative acts on your behalf, ask for a copy of every submission so your file stays complete. Clear records shorten calls, reduce repeat requests, and prevent missed deadlines.

Timing, Costs, and Payment Methods

Timeframes vary by case, but you control many of the delays. Clean files move faster than incomplete ones. Low-income certification can waive some fees. Payment method also affects cost and default risk, so choose the one you can maintain every month without drama.

Typical Review Timelines

Installment agreements can approve quickly when balances fit online limits. Offers in compromise take longer because the IRS verifies assets and income. CNC decisions depend on how fast you prove hardship with credible documents. Expect several months for complex cases and plan your cash flow around that reality. Keep all new filings current during review so your case does not stall.

Fees, Application Cost, and Waivers

The OIC application includes a fee and an initial payment unless low-income certification applies. Direct debit installment plans cost less to set up than non-automated plans. Some penalties can be reduced with first-time penalty abatement or reasonable cause, which lowers total cost before you choose a plan. Ask for written confirmation of any fee waiver. Keep receipts with your file.

Paying by Direct Debit, Payroll, or Credit Card

Direct debit reduces missed payments and helps avoid default. Payroll deduction agreements work well for W-2 earners who want a set-and-forget approach. You can pay taxes with a credit card through approved processors, but processing fees and card interest often cost more than IRS interest. Use a card only when you gain a real benefit and can pay the balance fast. For money orders or checks, mail early and save tracking data.

State Taxes, Refund Offsets, and Spouse Relief

Federal and state systems share ideas but run on different rules. You need a plan for both when you owe across agencies. Coordinate filings and budgets so one payment does not break the other.

Missouri and Other States Snapshot

Missouri and many states offer payment plans and hardship programs through their revenue websites. State taxes may file liens and start wage garnishments on a separate clock from the IRS. Share copies of your federal plan with the state when allowed, because many states mirror federal terms after you show eligibility income and qualifications. Check whether your state counts unemployment as gross income for payment testing. Document everything the same way you do for the IRS.

Overpayment, Injured Spouse vs Innocent Spouse

Overpayment usually offsets old balances before refunds reach your bank. If the overpayment comes from a joint return and the other spouse owes a separate debt, file an injured spouse claim so your share can be protected. Innocent spouse relief differs. It removes liability for a spouse who did not know about the item that caused the tax. Use spouse clearing explanations and provide proof of who managed the books and who benefited from the error.

Tax Lien Release, Withdrawal, Subordination

A release follows full payment or completion of an accepted offer. Withdrawal removes the public notice when you qualify under Fresh Start rules, often after you enter a direct debit plan and pay down the balance. Subordination lets a new lender take priority for a refinance when it helps you pay the IRS faster. Ask for the path that best fits your goal and timeline. Keep each approval letter in your records.

$1

If you prefer a done-for-you approach, our IRS Tax Relief team handles uploads and calls while you stay in control.

Web Application Walkthrough

Start in your Online Account and choose the feature that fits your goal. The offer tool estimates whether an OIC makes sense before you begin the full packet. It pulls in recent payments and shows deadlines. Use it to avoid paths that your numbers will not support. Save PDFs of every page you submit.

On Your Behalf by Representatives

A tax attorney or enrolled agent can link to your account after you authorize them. They will send forms, budgets, and attachments on your behalf, then share confirmation with you. Ask for a summary after each call so you know what the IRS requested next. One clear point of contact avoids crossed wires. Keep a shared checklist so nothing slips.

Status, Messages, and Uploads

Check account status weekly and after every submission. Respond to message center requests before the listed due date. Upload documents as clear scans with simple names that match the form line. When you mail instead, use certified mail and keep the receipt with your confirmation log. Good habits build momentum.

Real-World Scenarios and Case Playbooks

These playbooks show how facts drive different outcomes. Use them to set expectations and pick a strategy that fits your wallet and your goals.

W-2 Earner with Penalties

A W-2 filer owes for two years after under-withholding. First-time penalty abatement wipes one year of penalties after the filer sets a direct debit plan for the remaining balance. The budget shows room for a payment that clears the debt well within the collection period, so an installment agreement beats an offer. The filer updates the W-4 so no new balance forms. Clean filings for five years rebuild credit and peace of mind.

Self-Employed 25 Percent Drop

A sole proprietor shows a 25 percent revenue decline and high medical costs. The budget leaves little disposable income. The offer tool suggests an OIC based on low future income and minimal asset equity. The filer submits Forms 656 and 433-A/OIC with full backup, then makes periodic payments while the IRS reviews. If rejected, the same numbers support a partial payment installment agreement.

Small Business With Payroll Tax Debt

A restaurant owes payroll taxes after a cash crunch. Trust fund taxes do not disappear in bankruptcy and trigger fast enforcement. The owner enters a direct debit installment agreement and cuts nonessential costs to protect payroll deposits. The business explores lien subordination to refinance at a lower rate and free cash for payments. The owner posts weekly deposits on time to show good faith.

Appeals and Advocacy When Cases Stall

You have rights when you disagree with a decision or when a case sits without movement. Use them to keep control of the process and to get a fair review.

$1

For context on notice stages and deadlines, see our blog, IRS Collection Process Guide.

Taxpayer Advocate Service and TA Tax Diversity

Ask the Taxpayer Advocate Service to step in when delays pile for tax forgiveness or when you face economic harm. Advocates work across divisions and lift roadblocks that a single office cannot fix. Share proof of hardship, eviction risk, or medical needs. Keep your confirmations handy so they can see the full timeline. TAS does not replace the IRS, but it makes the system move.

When to Explore Bankruptcy Proceedings

Bankruptcy is a legal tool, not a shortcut. Some income taxes can discharge only when they meet the three-two-two-forty guideline. The return must be due for at least three tax years, filed for at least two years, and assessed for at least 240 days. Trust fund payroll taxes never discharge. Speak with counsel before you choose this path and weigh lien impacts and credit effects.

Get Help From Tax Hardship Center

At Tax Hardship Center, we help you choose the right relief path and then do the heavy lifting with the IRS. If a plan is best, we set it on direct debit and keep your filings current through our Installment Agreement and IRS Tax Relief services. If penalties inflate the total, we build a focused request through Penalty Abatement so the math works. When settlement fits, we prepare a thorough Offer in Compromise and guide you through each step to acceptance. You get clarity, steady updates, and a plan that respects your budget.

In summary…

The Fresh Start initiative groups proven relief options that help you handle IRS tax debt without guesswork. Use the right program for your numbers, document everything, and keep filings current so you stay eligible and protected. The path you choose should match your budget, your assets, and your goals over the next five years.

- Key relief options

- Installment agreement for predictable monthly payments

- Offer in compromise when assets and income cannot satisfy the full balance

- Currently Not Collectible status when payment would cause hardship

- Penalty abatement under first-time or reasonable cause rules

- Installment agreement for predictable monthly payments

- Application steps that keep cases moving

- File all missing returns and fix withholding or estimates

- Gather bank statements, pay stubs, housing and insurance details

- Choose the right program, complete the forms, and use your Online Account when possible

- Respond to IRS letters fast and keep copies of everything

- File all missing returns and fix withholding or estimates

- Outcomes and next moves

- Accepted offer requires five years of clean compliance

- Approved plan demands every payment on time and no new balances

- CNC pauses enforcement but interest and penalties continue

- A rejection leads to appeal, a revised offer, or a pivot to another option

- Accepted offer requires five years of clean compliance

Finish strong by keeping new taxes current, automating payments, and adjusting your budget so you never land back in collections. If your case gets complex, speak with a licensed professional who can review your documents and present your case clearly.

FAQs

What is a tax forgiveness program under Fresh Start?

A tax forgiveness program refers to IRS tools that reduce or settle tax debt: installment agreements, offers in compromise, penalty abatement, and currently not collectible status. These options fit different budgets and levels of hardship. You choose the path that matches your income, assets, and expenses. When you follow the rules and stay current, you can resolve the debt and protect your paycheck and bank account. Fresh Start is not a single form; it is a set of programs you use based on your facts.

Who qualifies for an offer in compromise?

You qualify when your reasonable collection potential falls below your tax debt and your documents prove it. The IRS looks at asset equity, household income, and necessary expenses, then tests whether it can collect more through normal methods within the collection period. If the numbers show that normal collection falls short, a settlement makes sense and the IRS can accept it. Low-income certification can waive the application fee and initial payment. You must file on time and stay current for five years after acceptance.

How do installment agreements work and what do they cost?

Installment agreements set a monthly payment and require a setup fee that drops when you choose direct debit and may be waived for low-income taxpayers. Interest and penalties continue until you pay the balance in full, so higher payments shorten the total cost. Many taxpayers can apply online and receive fast approval when balances and timelines fit published thresholds. If online tools do not fit, you can file Form 9465 by mail or request a plan by phone. Direct debit plans help you avoid default and reduce paperwork.

What happens if I cannot pay anything right now?

Ask for Currently Not Collectible status when payment would push you below basic living standards. You will document income, necessary expenses, and assets so the IRS sees that you cannot pay without hardship. CNC stops most enforcement while interest and penalties continue to add to the balance and the IRS may keep refunds. File on time and tell the IRS when your income rises, because the agency can revisit your case and restart collection if your ability to pay improves. CNC buys you time to stabilize and plan your next move.

How do I avoid tax relief scams?

Work only with licensed professionals and check every promise against the forms and rules you can confirm. Do not believe claims of automatic, one-time forgiveness without documents or math. Ask for a written scope of work that lists the forms, timelines, and fees, and walk away from anyone who guarantees acceptance of an offer. You can apply directly with the IRS for payment plans, offers in compromise, and penalty relief, and many reputable firms offer a free consultation to review your case. Trust the numbers, not the slogans, and keep control of your own IRS account.