A CP2000 notice can feel like the IRS is accusing you of doing something wrong. In reality, it is often a mismatch; your return did not match the information the IRS received from a third party, such as an employer, bank, brokerage, or payment platform.

The key is responding correctly and on time. When you handle CP2000 correctly, you can often fix errors, reduce the proposed amount, and prevent penalties from snowballing.

What A CP2000 IRS Notice Means

A CP2000 (sometimes written as CP 2000) is a proposed adjustment notice. The IRS sends it when third-party information does not match what you reported on your tax return.

Two important points:

- CP2000 is not a formal audit notice, nor is it a bill. It is the IRS proposing changes and asking you to agree or disagree.

- You may need to respond even if you think the IRS is wrong, because ignoring it can lead to escalation.

Your Deadline And Why Speed Matters

The IRS expects a response by the date listed on your notice. The IRS also states you should respond within 30 days of the notice date for faster resolution, or 60 days if you live outside the United States.

If you do not respond or the IRS cannot accept what you send, the IRS may issue a statutory notice of deficiency (often referred to as CP3219A), which is a more serious legal step.

What To Do First

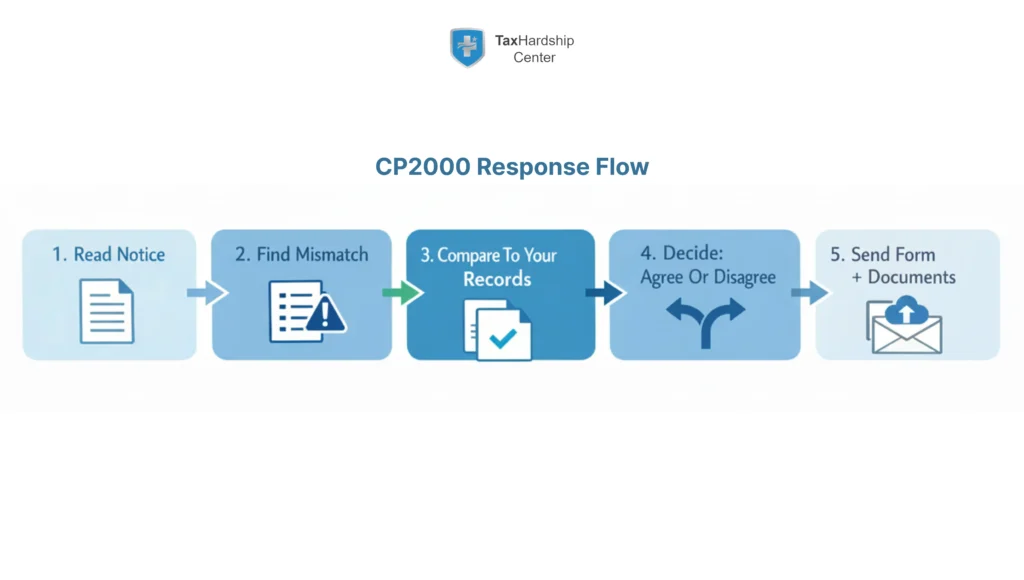

Confirm What The IRS Thinks Is Missing

Start by identifying exactly what line item triggered the mismatch. CP2000 usually lists the payer, the form type, and the amount the IRS matched against your return.

Pull Your Proof Before You Write Anything

Gather:

- The return you filed (and schedules)

- All W-2s and 1099s for that year

- Brokerage statements, transaction history, and cost basis support if investments are involved

- Business income and expense records if Schedule C is involved

- Any corrected forms (like a corrected 1099) if the payer reported something wrong

Choose Your Submission Method

The IRS says you can respond by uploading documents, faxing, or mailing to the address shown on the notice. Upload is often the fastest option when available.

Practical rule: do not send original documents, send copies.

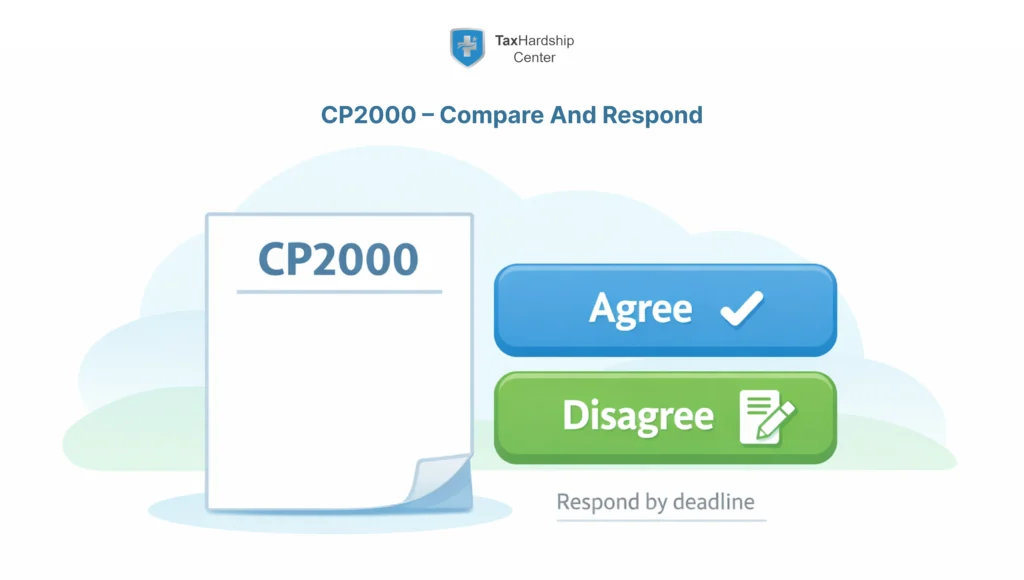

How To Respond If You Agree

If you agree with the proposed changes:

- Complete the response form, sign it, date it, and submit it by the due date.

- If you filed Married Filing Jointly, the IRS states both spouses’ signatures are required.

- If you agree and have no other changes, the IRS says you generally do not need to amend your return.

If you agree but cannot pay immediately, the IRS says you can apply for an installment agreement, but you still must return the signed response form by the due date.

How To Dispute A CP2000 And Lower The Proposed Amount

If you disagree with some or all of the changes:

- Mark the disagreement option on the response form.

- Include a signed statement explaining why you disagree.

- Attach supporting documentation.

- Submit by upload, fax, or mail to the location listed on the notice.

The Four Most Common Ways CP2000 Gets Overstated

1) The Income Is Yours, But The Tax Calculation Is Wrong

Example: investment sales reported on a 1099-B, but the cost basis is missing or incorrect, so the IRS proposal treats proceeds like profit. CP2000 is triggered by mismatches, and you can often reduce the proposed amount by providing the basis and transaction details.

2) The Income Is Reported Under Your SSN, But It Is Not Yours

This can happen due to payer error or identity issues. The Taxpayer Advocate Service specifically notes you may need to contact the third party and request that they correct what was reported to the IRS.

3) You Reported Net Income, The IRS Is Looking At Gross

This is common with self-employment, gig work, and payment platform reporting. Your records may show business expenses and net income, while the IRS is matching gross receipts from 1099s. CP2000 is a proposal; you can respond with documentation that supports the correct net figure.

4) You Actually Missed Income, But You Also Missed Deductions Or Credits

The IRS explains that if the CP2000 is correct and you have other income, credits, or expenses to report, you should file an amended return (Form 1040-X) and write “CP2000” at the top, then submit it with your response.

Dispute Package Checklist

Include only what supports the exact mismatch:

- A brief signed statement that references the notice number and tax year

- A one-page summary table tying the IRS proposed item to your proof

- Copies of corrected W-2/1099 (if available)

- Brokerage statements showing proceeds, basis, and dates

- Schedule C profit and loss and receipts (if self-employed)

- Any correspondence with the payer about a correction

What To Say In Your Statement

Keep it structured:

- Identify the CP2000 tax year and the exact item you dispute.

- State the correct amount and why.

- List the documents attached and what each proves.

- If the payer made an error, state that you requested a corrected form and include proof.

If you want to preserve appeal options, the IRS indicates that CP2000 is a notice offering an appeal opportunity, and the general guidance describes a 30-day protest timeline from the letter date for Appeals.

How To Reduce Penalties And Interest

Interest

The IRS explains CP2000 interest is generally calculated from the return due date to about 30 days from the notice date, and interest continues to accrue until the amount is paid in full. Paying within 30 days can stop additional interest and possibly additional penalties from accruing.

Accuracy-Related Penalties

The IRS explains that the accuracy-related penalty is generally 20% of the portion of an underpayment attributable to negligence or substantial understatement, and the IRS may send a notice if you owe it.

If you received an accuracy-related penalty, the IRS states you may qualify for penalty relief if you acted with reasonable cause and good faith, considering factors like your efforts to comply, complexity, and reliance on a qualified advisor.

Practical approach: contest the penalty early in your CP2000 response when you have facts that support reasonable cause and good faith, instead of waiting for later stages.

Payment Options If You Owe After CP2000

If the IRS ultimately assesses a balance:

- You can pay in full, or

- You can request an installment agreement (payment plan).

If you agree with the proposed amount, the IRS says you can pay right away online, or wait for the IRS to adjust your account and send a bill, but waiting means interest keeps accruing.

What Happens If You Ignore CP2000

Ignoring CP2000 is where people lose leverage.

The IRS states that if you do not respond or if it cannot resolve the discrepancy, it may send another notice and a bill.

The IRS also explains that if it does not hear from you by the response date, it will send a statutory notice of deficiency.

Once you are at the deficiency stage, timelines and options tighten significantly, and it becomes much harder to resolve with a simple documentation package.

When To Call A Professional

CP2000 is “fixable,” but it can also be deceptively technical. Consider professional help if:

- The notice involves investments, crypto, basis, or multiple transactions.

- You are self-employed, and the IRS is treating gross deposits as taxable income.

- The income is not yours, and you need to build a clean record to correct it.

- Penalties are proposed, and you need a reasonable-cause strategy.

- You are close to the deadline and cannot risk a sloppy response.

FAQs

Is CP2000 An Audit Or A Bill?

CP2000 is not a formal audit notice, nor is it a bill. It is a proposed adjustment notice asking whether you agree or disagree.

Do I Need To Amend My Return If I Agree?

If you agree and have no other changes, the IRS says you generally do not need to amend your return.

What If I Agree With The Change But I Have Other Deductions To Add?

The IRS says if the CP2000 is correct and you have other income, credits, or expenses to report, file Form 1040-X, write “CP2000” on top, and submit it with your response.

What If The Income Reported Does Not Belong To Me?

The Taxpayer Advocate Service notes that you may need to contact the third party and request that the information reported to the IRS be corrected, then submit supporting documentation with your response.

What Happens If I Miss The CP2000 Deadline?

The IRS states that if it does not hear from you by the response date, it will send a statutory notice of deficiency.

Conclusion

A CP2000 notice is often a mismatch problem, not a fraud accusation. The fastest way to protect yourself is to treat it like a documentation project with a deadline. Confirm the mismatch, decide whether you agree, and send a clean response package through the method the IRS provides (upload, fax, or mail).

When you disagree, focus on proof, not emotion. CP2000 disputes are won with records that clearly tie the proposed change to the correct number, especially in common overstatement cases like missing cost basis, gross-versus-net reporting, or third-party reporting errors.

Key Takeaways:

- CP2000 is a proposed adjustment, not a bill, and you must respond by the date on the notice (usually 30 days, 60 if outside the U.S.).

- If you agree, sign and return the response form; you usually do not need to amend it.

- If you disagree, submit a signed explanation plus supporting documents, and use Form 1040-X with “CP2000” on top if you need to add missing deductions or credits.

- Interest can continue to accrue, and paying within 30 days may prevent additional interest and possibly penalties from accruing.

- If penalties are proposed, you may be able to request relief based on reasonable cause and good faith when supported by facts.