A CP90 notice is not an informational reminder. It is the IRS telling you that levy action is on the table, and your time to protect yourself is limited.

If you respond quickly and choose the right path, you can often stop enforcement before it hits your paycheck, bank account, or other assets. This guide breaks down what CP90 means, what to do next, and the last-chance options that typically work.

What Is The IRS CP90 Final Notice

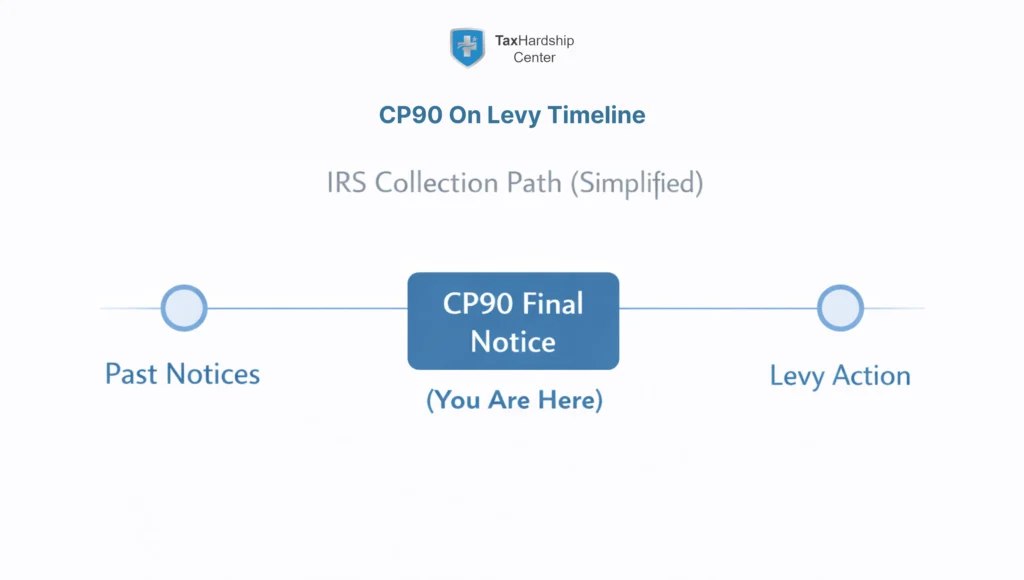

CP90 is a “Final Notice, Notice of Intent to Levy and Notice of Your Right to a Hearing.” In plain terms, the IRS is warning that it intends to levy property or rights to property to collect unpaid taxes, and it is notifying you of your right to request a Collection Due Process hearing.

What Can The IRS Levy After CP90

The CP90 notice itself lists examples of property or rights to property that may be levied if you do not respond, including wages, bank accounts, business assets, personal assets (like a car or home), state tax refunds, and Social Security benefits.

Why CP90 Often Shows Up

CP90 is also commonly used as the pre-levy notice tied to the Federal Payment Levy Program, where the IRS matches delinquent accounts against federal payments you are due. If you do not respond within 30 days, the IRS may transmit the levy electronically to the Bureau of the Fiscal Service.

Why CP90 Is Urgent

You Are On A Short Clock

IRS and Appeals guidance consistently tie CP90 to a 30-day window for requesting a CDP hearing using Form 12153.

Levy Action Can Affect Real-Life Cash Flow

Under the Federal Payment Levy Program, certain federal payments can be reduced by 15% (or more in some special cases), and the levy can be continuous until the debt is resolved or arrangements are made.

Passport Issues May Also Be In Play

The CP90 notice and IRS CP90 guidance also warn that seriously delinquent tax debt can trigger passport restrictions under federal law, which is another reason not to let this sit unopened.

Immediate Actions To Take (First 24 Hours)

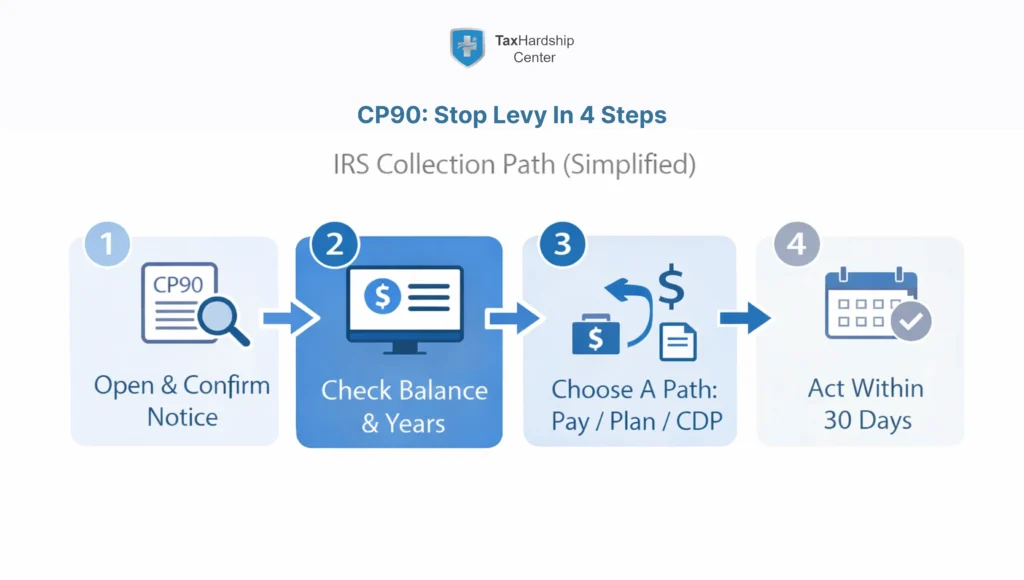

1) Verify The Notice And Mark Your Deadline

Confirm the notice number (CP90) and locate the response date shown on your letter. Do not rely on memory or assumptions, because the date on the notice drives your next steps.

2) Confirm What Years And Balances Are Involved

Your notice includes the tax period(s) and totals. Pull your recent IRS letters and any payment confirmations so you can speak clearly when you contact the IRS or submit a response package.

3) Choose Your Goal Before You Call Or File Anything

Most CP90 cases fit one of these goals:

- You can pay the balance (or most of it) immediately.

- You need a payment plan.

- You need a hearing to stop the levy action while you propose a resolution.

4) Avoid “Half-Moves” That Waste Time

At the CP90 stage, your best results usually come from one decisive action: pay, get a plan approved, or file a timely hearing request.

Last-Chance Options To Stop A Levy And Secure A Resolution

Option 1: Pay In Full (Fastest Way To End The Threat)

If paying in full is realistic, it closes the collection risk fastest. The IRS CP90 guidance directly instructs taxpayers to pay what they owe.

Option 2: Set Up A Payment Plan (Most Common Resolution)

If you cannot pay in full, a payment plan is often the cleanest way to stabilize the account and reduce the risk of escalation. IRS CP90 guidance points taxpayers to request a payment plan if they cannot pay the full amount.

Related internal reads:

Option 3: Offer In Compromise (Only When You Qualify)

The IRS CP90 guidance highlights Offer in Compromise as a potential option to explore. This path is not a shortcut; it is a qualification-based program where the IRS evaluates the ability to pay.

Option 4: Request A Collection Due Process Hearing (Strongest “Stop Enforcement” Tool)

A timely CDP request is often the best way to pause levy pressure while you present an alternative, like an installment agreement or settlement. CP90 is specifically listed by the IRS as a notice that offers an appeal opportunity through Form 12153, filed within 30 days.

Option 5: Use IRS Representation If The Case Is Escalating

The IRS CP90 page specifically references Form 2848 (Power of Attorney) if you want a qualified representative to communicate with the IRS on your behalf.

How To Request A Collection Due Process Hearing (Step By Step)

Step 1: Use Form 12153

Form 12153 is the IRS form used to request a Collection Due Process or Equivalent Hearing for notices like CP90.

Step 2: Submit It The Way The IRS Accepts For Your Notice

The IRS CP90 guidance says you can submit documents using the IRS Document Upload Tool with the access code located on your notice, or mail your documents to the address on your notice if you cannot use the upload tool.

Step 3: Be Clear About What You Are Requesting

In your request, it helps to clearly state what outcome you want the Appeals Office to consider, such as:

- An installment agreement payment plan you can afford

- An Offer in Compromise if you qualify

- A collection alternative based on financial hardship

The Taxpayer Advocate Service notes that the intent-to-levy notice exists to give you the right to request a CDP hearing before levy in most situations, unless an exception applies.

Step 4: Keep Proof Of Submission

Keep copies of everything you submit, plus upload confirmations or mailing proof. At this stage, documentation is leveraged.

What Happens If You Ignore CP90

If you do not pay, make arrangements, or request a hearing by the date on the notice, the IRS may proceed with levy action. The CP90 notice describes the levy as the seizure of property or rights to property and lists examples such as wages, bank accounts, and other assets.

Separately, CP90 can tie into federal payment levies. Under the Federal Payment Levy Program, if the IRS does not hear from you within 30 days, it may transmit the levy electronically to reduce eligible federal payments.

Missed The Deadline? Backup Options

If your CDP request is not timely, you may still be able to request an Equivalent Hearing within one year from the date of the notice, but the rights are different, including limits on going to Tax Court if you disagree with the decision.

This is still worth pursuing if you need an appeals review, but it is best to act as if you are still within the 30-day window until you confirm otherwise.

FAQs

Is CP90 The Same As LT11 Or Letter 1058

They are all “intent to levy” notices that provide CDP hearing rights, but they are not identical letters. The Taxpayer Advocate Service lists CP90, LT11, and Letter 1058 as examples of intent-to-levy notices that carry CDP rights.

How Long Do I Have To Respond To A CP90 Notice

IRS Appeals guidance describes CP90 as a notice where you should file Form 12153 within 30 days from the date of the letter to appeal the proposed levy action.

Can CP90 Lead To Wage Garnishment Or A Bank Levy

Yes. The CP90 notice lists wages and bank accounts among the property or rights to property that may be levied.

Helpful internal reads:

Stop IRS Wage Garnishment

IRS Bank Account Levy

Does CP90 Affect Social Security Or Other Federal Payments

It can. The CP90 notice lists Social Security benefits as a potential levy target, and the Federal Payment Levy Program explains that certain Social Security benefits and other federal payments may be subject to levy.

Do I Need A Professional To Respond To CP90

Not always, but it is strongly worth considering if you are close to deadlines, have multiple tax years, need a hardship-based alternative, or expect levy action to hit wages, bank accounts, or federal payments.

Conclusion

CP90 is a last-chance notice because it sits right before levy action and because your appeal rights are time-sensitive. The best move is the one that gets you into an approved resolution quickly, with proof, and without missed deadlines.

Key Takeaways:

- CP90 is a final intent-to-levy notice and includes your right to request a CDP hearing.

- Treat CP90 like a 30-day clock: pay, set up a plan, or file Form 12153 on time to protect your rights.

- CP90 can lead to levies on wages, bank accounts, and other assets, and it may also connect to federal payment levies.

- If you missed the timely window, an Equivalent Hearing may still be available, but you lose important protections.

- If enforcement risk is high or deadlines are tight, IRS representation (including the use of Form 2848) can reduce errors and speed up resolution.